Are you looking for investments that can truly outperform the broader market and deliver highly focused returns? If so, then understanding Thematic Mutual Funds in India32% Returns in Last 5 Years (Outperforming)” is essential. These funds have proven their potential by targeting powerful, future-ready sectors, with many schemes delivering up to an astonishing 32% returns over the last five years. However, navigating the many available options can be a challenge. In this guide, we cut through the confusion to present the Top 7 Thematic Mutual Funds in India that have consistently beaten their peers, helping you answer three core questions:

1. Theme-Based Investing – These funds focus on a specific sector or theme (like Technology, Banking, Energy, or Healthcare).

2. High Risk–High Return –

When the theme performs well, returns can shoot up to 30–35% CAGR, but the downside risk is equally high.

3. Best for 3–5 Years Horizon – Suitable

Suitable for short to medium-term growth opportunities, not ideal for long-term core portfolios.

4. Diversification Tip

Limit exposure to 5–10% of your portfolio to capture growth while keeping risks under

1 :Technology Thematic Fund 🚀

💡 Objective: Invests in fast-growing IT, cloud, AI, and digital businesses shaping the future.

📊 Annualised Returns:

1 Year: 8.5%3 Years: 15.7%5 Years: 21.3%

👤 Who Should Invest:

Long-term investors betting on India’s tech boomRisk-takers looking for high growth in Thematic Mutual Funds in IndiaThose comfortable with short-term volatility⚠️ Risks: Rapid tech disruptions • High volatility • Sector-only exposure

Investors wanting a defensive sector in their portfolioThose looking for steady growth in Thematic Mutual Funds in IndiaLong-term healthcare believers

⚠️ Risks: Regulatory hurdles • High R&D costs • Drug approval delays

3. Infrastructure Thematic Fund 🏗️

💡 Objective: Focuses on roads, power, and India’s mega-development projects.

📊 Annualised Returns:

1 Year: 9.4%3 Years: 17.8%5 Years: 23.6%

👤 Who Should Invest:

Long-term wealth creators (5+ years)Investors betting on India’s growth storyThose seeking higher returns from Thematic Mutual Funds in India

⚠️ Risks: Policy risks • Project delays • High capital exposure

4 Banking & Financial Services Fund 💳

💡 Objective: Invests in banks, NBFCs, insurance & fintech companies.

📊 Annualised Returns:

1 Year: 7.1%3 Years: 16.2%5 Years: 22.4%

👤 Who Should Invest:

Those seeking growth + dividend potential Investors wanting core exposure to India’s financial backbone Thematic Mutual Funds in India lovers focusing on BFSI sector

✅ Conclusion: Thematic Mutual Funds allow investors to ride on specific megatrends like technology, healthcare, and infrastructure. They can deliver 32%+ returns over 5 years, but come with higher risk & volatility compared to diversified funds. Hence, investors should pick them as a satellite allocation (10–20% of portfolio), not as the core portfolio.

Call To Action

✅ Invest Smart, Grow Faster with Thematic Mutual Funds! 🚀 👉 Explore Top Thematic Funds Now 💹 🔎 Discover High-Risk, High-Reward Mutual Funds Today! 📊 📢 Don’t Miss – Top 7 Thematic Mutual Funds in India! 🌍

iam content writer ihve experience and expertise 3 year

Asif Khan

what is flexi cap

FlexiCap Funds are a type of mutual fund that invest across large-cap, mid-cap, and small-cap stocks. These funds give fund managers the flexibility to pick the best stocks based on market conditions. This makes them an ideal choice for middle-class families, offering the potential for 12–15% growth over 5 years while keeping investments diversified.

History of flexicap

FlexiCap Funds are a relatively new type of mutual fund.

Earlier, mutual funds had fixed allocation rules – you had to invest a certain % in large-cap, mid-cap, or small-cap stocks.

FlexiCap Funds were introduced to give fund managers flexibility, allowing them to adjust investments dynamically across all market caps depending on market trends.

Over the last 5–10 years, these funds have become popular among middle-class investors, offering both diversification and good growth potential.

Parag Parikh Flexi Cap Fund is a premium global flexi-cap mutual fund available to investors in India. 🌍 It invests across a wide spectrum of stocks, including large-cap, mid-cap, and small-cap companies, both domestically and internationally. Its primary goal is long-term wealth creation, providing investors exposure to global markets. By combining domestic and international opportunities, this fund allows for portfolio diversification, aiming to balance risk and reward effectively over time.

Key Highlights

This fund follows a value and growth-oriented investment strategy, carefully selecting stocks with strong potential for long-term appreciation. It is particularly suitable for middle-class investors who want to build wealth gradually. Over the last 5 years, the fund has delivered approximately 21.43% CAGR (Check on Moneycontrolhttps://www.monnycontrol.com), making it a consistent performer in its category. Investors benefit from diversification across market caps and exposure to Indian and global equities, which helps balance risk and growth potential.

Why Choose This Fund

Investors prefer Parag Parikh Flexi Cap Fund because it offers a balanced risk-return profile through strategic allocation across domestic and international stocks. Managed by experienced fund managers, the fund emphasizes long-term sustainable growth. With an average 5-year return of 21.43%, it is ideal for investors seeking a well-diversified portfolio, a global perspective, and consistent performance. Its unique blend of value and growth stocks ensures a comprehensive strategy for wealth creation over the years. 💼They Ignored You When You Were Broke — Now They Watch in Silent Jealousy

2. Mirae Asset Flexi Cap Fund

📈 5-Year ReturnThe Mirae AssetFlexi Cap Fund has delivered an impressive ~20% CAGR over the past five years.👉 For example, if someone had invested ₹1,00,000 in 2019, today that amount would have grown to ₹2,48,800+ in 2024. This shows the fund’s power in compounding and wealth creation.

💡 Investment Strategy

The fund primarily invests in Indian equities with a focus on high-growth sectors like Banking, IT, Healthcare, and Consumer Goods. By spreading investments across large-cap, mid-cap, and small-cap stocks, it ensures a balanced mix of stability and aggressive growth. This helps middle-class investors enjoy the growth of India’s economy while minimizing risk from market fluctuations.Best Investment Options for Beginners in India (2025 Guide)

👨👩👧 Ideal For

This fund is ideal for salaried professionals and middle-class families aiming for long-term wealth creation. Even a small SIP of ₹5,000 per month for 5 years could have grown to ₹4.5–5 Lakh+, compared to only ₹3 Lakh invested. This makes it a powerful tool for achieving life goals like children’s education, home purchase, or retirement planninghttps://www.moneycontrol.com/

. #3 JM Flexi Cap Fund

1. Diversified Across Market CapsJ M Flexi Cap Fundinvests in large-cap, mid-cap, and small-cap stocks, allocating funds dynamically based on market trends. For example, if the fund has ₹500 crore invested in large-cap stocks, it might allocate ₹300 crore to mid-cap and ₹200 crore to small-cap to balance risk and returns.

Sectoral Flexibility

The fund shifts investments across sectors like technology, finance, healthcare, and consumer goods depending on growthopportunities. This flexibility allows ₹100–₹200 crore to move into high-growth sectors without affecting overall portfolio stability.https://www.moneycontrol.com/

Dynamic Risk Management

JM Flexi Cap Fund adjusts its portfolio according to market volatility. During uncertain times, the fund may increase allocation to safer large-cap stocks and reduce exposure in small-cap stocks, ensuring that the investor’s ₹1 lakh SIP or ₹5 lakh lump sum is protected while still aiming for growth.“7 Proven Ways for Small-Town Students to Earn Money Online in 2025 (₹5k–₹50k/Month)”

4. Quant Flexi Cap Fund 🚀

This fund is a flagship offering known for its dynamic and aggressive investment strategy, frequently ranking among the top performers in the Flexi Cap category. It is an ideal choice for investors with a high-risk appetite aiming for accelerated long-term capital growth.

Investment Strategy & Philosophy

The Quant Flexi Cap Fund relies heavily on a Quantitative (Quant) model which uses predictive analytics and market signals, rather than traditional research, to actively manage its portfolio. The fund managers use a flexible approach, aggressively shifting allocation across large, mid, and small-cap stocks based on their proprietary VLRT (Valuation, Liquidity, Risk, and Time) framework. This high-conviction, concentrated approach allows the fund to swiftly capitalise on market volatility and capture significant growth opportunities.

Performance and Key Figures

The The fund has demonstrated sorryty check 🔗http://Quant Flexi Cap Fund Direct-Growth – Latest NAV, Returns, Performance 2025Source: exceptional compounding ability, delivering a high 5-year CAGR of approximately 27.9\%. As of the latest data, its Assets Under Management (AUM) stand at around ₹6,686.67 Crores. An investor can start a Systematic Investment Plan (SIP) with a minimum amount as low as ₹250, making it accessible to most middle-class savers aiming for high returns. has demonstrated exceptional compounding ability, delivering a high 5-year CAGR of approximately 27.9\%. As of the latest data, its Assets Under Management (AUM) stand at around ₹6,686.67 Crores. An investor can start a Systematic Investment Plan (SIP) with a minimum amount as low as ₹250, making it accessible to most middle-class savers aiming for high returns.7 Proven Ways for Students to Make Money

5 PGIM India Flexi Cap Fund 📊

This fund has rapidly gained recognition for its consistent, risk-adjusted returns and a structured investment process focused on generating alpha across market cycles. It appeals to investors seeking a balance of aggressive growth potential and strong downside protection.https://www.pgimindia.com/mutual-funds/equity-funds/flexi-cap-fund

Investment Strategy & Philosophy

The PGIM IThe PGIM India Flexi Cap Fund adheres to a disciplined GARP (Growth at a Reasonable Price) philosophy. The fund managers focus on identifying high-quality businesses with strong governance and a proven track record of earnings growth, but only when they are available at attractive valuations. The strategy involves a rigorous 3-step investment process—Idea Generation, Fundamental Research, and Portfolio Construction—ensuring that capital allocation is based on deep analysis rather than market sentiment. This balanced approach helps the fund remain resilient during volatile market phases.adheres to a disciplined GARP (Growth at a Reasonable Price) philosophy. The fund managers focus on identifying high-quality businesses with strong governance and a proven track record of earnings growth, but only when they are available at attractive valuations. The strategy involves a rigorous 3-step investment process—Idea Generation, Fundamental Research, and Portfolio Construction—ensuring that capital allocation is based on deep analysis rather than market sentiment. This balanced approach helps the fund remain resilient during volatile market phases.

Performance and Key Figures

The fund has demonstrated its efficacy by delivering a robust 5-year CAGR averaging around 21\%, positioning it well above the category average. The total size of the fund, or its Assets Under Management (AUM), currently stands at approximately ₹8,500 Crores (Note: AUM figures are subject to daily market fluctuations). For investors initiating a Systematic Investment Plan (SIP), the minimum investment requirement is generally ₹1,000, making this high-quality, high-growth fund accessible to a wide range of investors.Best Investment Options for Beginners in India (2025 Guide)

The fund employs a rigorous bottom-up stock selection approach, primarily focusing on acquiring high-conviction, quality stocks irrespective of their market size (large, mid, or small-cap) or sector. The fund seeks out companies with solid fundamentals, experienced management, and a high potential for compounding wealth over a long period. This disciplined, long-term approach makes it suitable for conservative investors with an investment horizon of five years or more. The portfolio is often seen as less volatile than many of its aggressively managed peers.

Performance and Key Figures

Known for its consistent performance across various market cycles, the fund has given a respectable 5-year CAGR of approximately 18.16\%. It is one of the largest funds in the Flexi Cap space, managing substantial Assets Under Management (AUM) of roughly ₹25,500 Crores. You can initiate a SIP in this quality-focused fund with a minimum monthly investment as low as ₹500. Sorsehttps://www.utimf.com/mutual-funds/uti-flexi-cap-fund-formerly-known-uti-equity-fund

Call To Action

Click 📌 Call to Action 💡 Looking for steady long-term growth? FlexiCap Funds can give you 12–15% returns in 5 years. Perfect for middle-class families aiming for wealth building. 👉 Start investing today and secure your financial future!

🚀 Don’t let your savings sit idle! FlexiCap Funds deliver consistent growth with smart strategies. With 12–15% 5-year performance, your money works harder for you. 👉 Invest now and achieve your financial goals faster!

Living in a small town no longer limits your dreams. In 2025, students can easily earn ₹5k–₹50 k/month online using proven methods. From freelancing to content creation and even digital products, opportunities are everywhere. In this guide, you’ll discover 7 powerful ways to start making money online — without leaving your hometown!

Skills: WRITING, GRAPHIC DESIGN, WEB DEVELOPMENT, SEO, DATA ENTRY.Platform: Upwork, Fiverr, Freelancer.Earnings: ₹5,000–₹15,000/month 💙 (Beginner), ₹20,000+/month 💙 (Experienced).Example: 10 articles per month x ₹500 per article = ₹5,000/month 💙.

Skills: Market research, Art creation (for NFTs).Platform: Binance, coindtx OpenSea.Earnings: Variable, from ₹5,000 to ₹100,000+ 💙 (High Risk).Example: A small crypto 💙 investment of ₹5,000 could increase to ₹10,000 in a few months if the market goes up.More knowledge http://Proven Ways for Students to Make Money ‣ paisakmao.de https://

5. Online Tutoring 💙

Skills: Expertise in a specific subject (Math, Science, English, etc.).

Platform:Chegg Tutors, TutorMe, private clients.

Earnings:₹300–₹800/hour 💙.

Example: Tutor 10 hours a week x ₹500/hour = ₹20,000/month 💙.

6. Social Media Management

Social Media Management 💙Skills: Content planning, Community engagement, Analytics.Platform: Instagram, Facebook, LinkedIn.Earnings: ₹5,000–₹15,000/month 💙 (per client).Example: Manage 2 small business accounts x ₹7,500/month = ₹15,000/month 💙.

7.Affiliate Marketing

Affiliate Marketing 💙Skills: Content creation (reviews, guides), Audience building.Platform: Amazon Associates, Flipkart Affiliate, or other company programs.Earnings: ₹2,000–₹25,000+/month 💙 (based on sales).Example: Drive 10 sales a month for a product worth ₹2,000 with a 10% commission = ₹2,000/month 💙.

Quick Summary – 7 Proven Ways to Earn Online

1. Freelancing – Sell your skills on platforms like Fiverr or Upwork. 2. Content Creation – Start a YouTube channel, blog, or podcast to monetize your content. 3. Digital Products – Create eBooks, courses, or templates and earn passive income. 4. Crypto & NFTs – Invest wisely in trending digital assets for future gains. 5. Online Tutoring – Teach students online and earn from your knowledge. 6. Social Media Management – Help businesses grow their online presence. 7. Affiliate Marketing – Promote products and earn commission per sale.

Call To Action

Click here .earn money online 2025 – 👉 Start today! make money online for students – 👉 Begin your journey now! freelancing for beginners – 👉 Get your first project! content creation 2025 – 👉 Create & earn! digital products selling online – 👉 Launch today! crypto and NFTs income – 👉 Explore & invest! online tutoring jobs – 👉 Teach & earn! affiliate marketing for students – 👉 Promote & profit!

INTRODUCTION When your income is low, saving money feels impossible.You earn little, bills are many, and by the end of the month, nothing is left.I have been in this situation. Here, you will learn how to save money when income is low, using simple habits, real-life thinking, and practical steps — no complex finance words.…

íntroduction Best Zero Balance Savings Account for Students in India (2026 Guide) In today’s digital era, every student needs a bank account to manage scholarships, pocket money, and UPI payments. However, most traditional banks require a high “Monthly Average Balance” (MAB), which is often impossible for a student to maintain. If you are searching for…

1. Introduction: What Are ETFs & Mutual Funds? Investing doesn’t have to be complicated — two of the most common ways to invest are ETFs (Exchange-Traded Funds) and Mutual Funds. Both pool money from many investors to buy a basket of securities like stocks or bonds, but how you buy them, cost, taxation, and flexibility…

introduction Best Saving Schemes for Middle Class Family (India. Saving money wisely is one of the most important financial habits for a middle-class family in India. With rising inflation and increasing expenses, having a clear plan for saving and investing can secure your family’s future. This guide covers top saving schemes for 2025, tailored specifically…

introduction Post Office Saving Schemes for Middle Class – Complete GuideFor a middle-class family in India, the biggest financial priorities are safety, stable returns, and long-term security. Not everyone is comfortable with stock market risk or private investment products. This is where Post Office Saving Schemes become a trusted, government-backed solution.In this article, you will…

Introduction Saving money is not about cutting every expense — it’s about small, consistent habits that grow over time.The most viral and effective saving method in 2025 is the 52 Week Money Challenge. This simple but powerful challenge helps you build a strong saving habit without stress, without strict budgeting, and without big income. Let’s…

introduction 10 Easy Ways to Make Money at Home” is not just a topic today, it has become a real need. Many people want to earn money from home — students, housewives, working professionals, and beginners. The good news is, with just a smartphone and an internet connection, there are several simple and practical ways…

Introduction Investing in mutual funds is becoming Top High-Return Mutual Funds for 2026 (AI-Predicted Expertone of the smartest and safest ways to build long-term wealth in India. As we move towards 2026, millions of new investors are entering the market with the goal of achieving higher returns, lower risk, and stable long-term growth. But with…

intoductionAre you a student struggling with money but too busy to take a full-time job? Don’t worry — you’re not alone. The good news is, there are smart and proven ways to make money even if you’re broke and have limited time. In this post, we’ll explore 7 practical methods students can use to start…

In today’s fast-paced life, having a steady monthly income is crucial. Investing in the right schemes can help you earn ₹5,000, ₹10,000, or more every month while keeping your money safe. These monthly income schemes provide fixed and reliable returns, helping you manage expenses and secure your financial future. Here are the top 7schemes to start earning consistent monthly income.

Higher Interest Rate SCSS generally offers around 8.2% p.a. (2025 rate approx). For example, if you invest ₹1,00,000, you can earn about ₹8,200 per year as interest. Bigger deposits like ₹10 Lakh can generate ₹82,000 yearly.

#2Quarterly Payouts

The interest is credited every 3 months. So, on an investment of ₹1,00,000, you get around ₹2,050 every quarter. This acts like a steady pension for senior citizens.

3. Government-Backed Safety

Since SCSS is a government scheme, your capital is 100% safe. Even if banks or private firms fail, your ₹1 Lakh or more investment remains fully secure.

4. Capital Protection

At the end of the maturity period (5 years, extendable to 8 years), your full deposit (say ₹1,00,000) is returned along with all the interest you earned during the years.

#2Post Office Monthly Income Account (POMIA)

By depositing ₹50,000 to ₹4,50,000, you can earn a fixed monthly interest. For example, a deposit of ₹1,00,000 could give you approximately ₹750–₹800 per month. Your principal is safe, and you enjoy a regular income without any hassle.

2. Monthly Income Scheme (MIS)

The Monthly Income Scheme allows you to deposit ₹1,500 to ₹4,50,000 and get monthly income directly into your account. For example, a ₹2,00,000 deposit can provide around ₹1,000 per month, making it ideal for pensioners or small investors.

3. Kisan Vikas Patra (KVP)

Invest ₹10,000 or more in KVP and watch it grow over the fixed tenure. While the maturity amount comes after a few years, it can be used to generate regular monthly income, roughly ₹500–₹1,000 per month, depending on your planning. This is great for farmers or small investors seeking safe returns.

4. Sukanya Samriddhi Yojana (SSY

Invest ₹1,000 to ₹1,50,000 annually in SSY for your daughter’s future. The scheme accrues interest and can be planned to provide monthly financial support later. For example, a cumulative investment of ₹2,00,000 can give a monthly benefit of ₹1,500–₹2,000, securing both savings and regular income.

Corporate FDs are issued directly by companies instead of banks. You have to invest through the company’s office or authorized partners, which often helps you get higher interest rates compared to bank deposits.

2Income Alone

This scheme is designed to provide a steady monthly income. For example, if you invest ₹5,00,000, at an 8–10% annual interest rate, you can earn around ₹3,500–₹4,200 every month.

3 Monthly Payout Option

Corporate FDs allow you to choose payout frequency—monthly, quarterly, or yearly. If you select the monthly option, the company credits a fixed amount to your account every month, ensuring regular income.

4 Higher Returns

Compared to bank FDs, corporate FDs generally offer higher returns. However, they carry slightly more risk since repayment depends on the company’s financial health. Always choose AAA or high-rated companies for safer investments.How to Save Money as a Student: Beginner Guide in 2025

#4 Corporate Fixed Deposits

Corporate Fixed Deposits (FDs) are investment instruments issued by companies that can offer higher returns than bank FDs. Here is the information presented professionally with numbered points and financial figures:

1Higher Returns: Corporate FDs

offer a 1% to 3% higher return compared to bank FDs. For example, a bank FD might offer a 6.5% return, while a corporate FD could yield 8.5%.fds

Monthly Income Option: Many corporate

FDs provide a monthly payout option. If you invest ₹5,00,000 at an annual return of 8.5%, you could receive a fixed mounthly income of approximately ₹3,542

3Investment & Risk:

: It is essential to check a company’s credit rating before investing. Companies with high ratings like AAA or AA+ are considered the safest. However, they always carry slightly more risk than bank .fds.

Investment Amount & Term:

start investing in corporate FDs with amounts as low as ₹5,000 and can choose a term from 1 to 5 years as per your convenience.

Conclusion:

Corporate FDs are a good option for investors who seek returns higher than bank FDs and are willing to take on a moderate level of risk.easy money for busy students

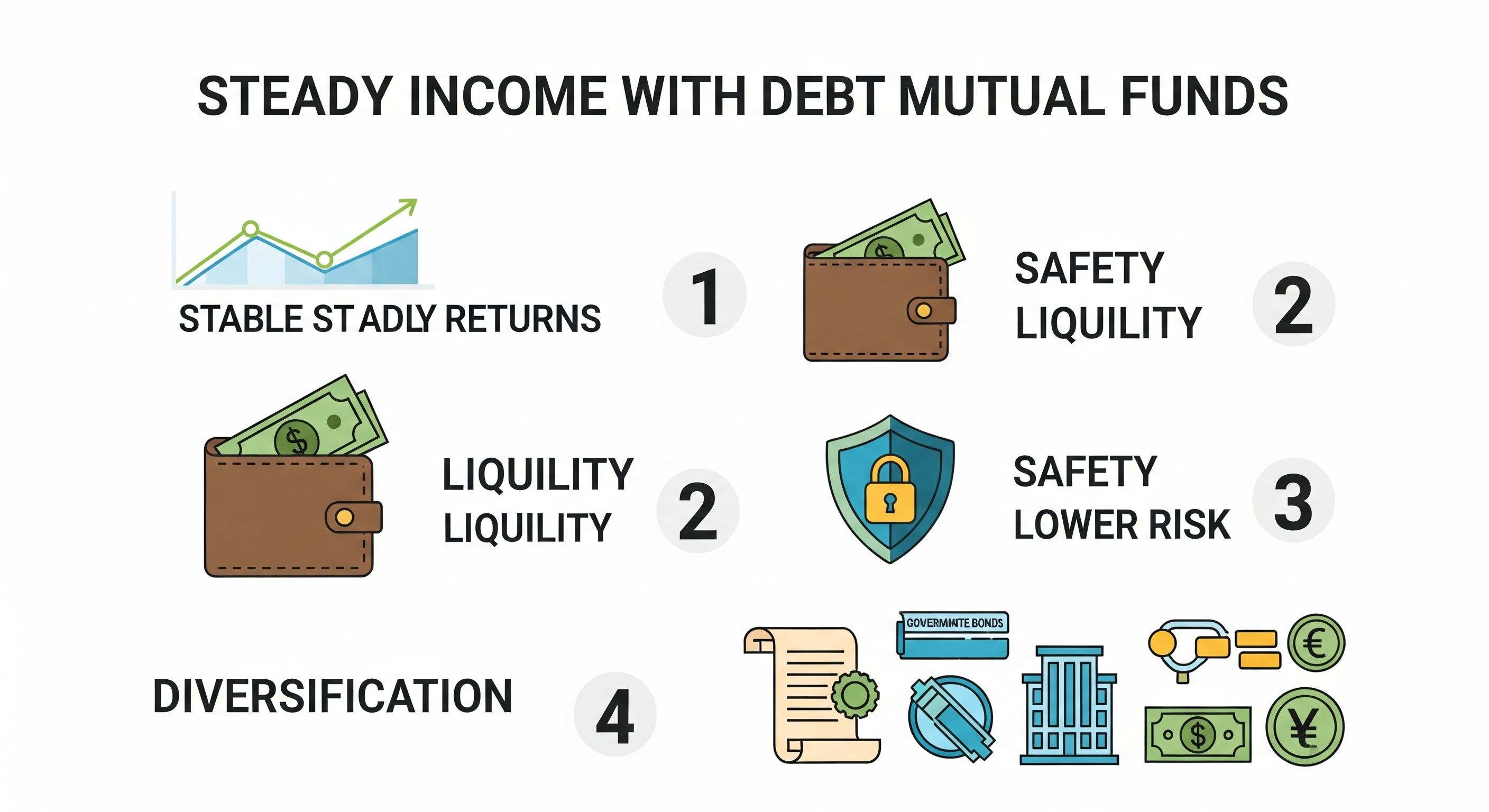

#5Debt Mutual

Mutual Funds:Steady Income: Debt Mutual Funds aim to provide a steady income stream by investing in fixed-income securities like bonds. This makes them a great option for investors who are looking 1for a regular return without the volatility of the stock market.

2 Safety AND Risk

Safety and Risk: They are generally considered safer and less risky than equity (stock) funds. While they are not risk-free, they offer a good balance between safety and returns, making them a suitable choice for conservative investors.

3High Liquidity

Unlike fixed deposits that have a lock-in period, most Debt Mutual Funds offer high liquidity. This means you can easily withdraw your money at any time, often within 1-3 working days, without any penalty.Best Investment Options for Beginners in India (2025 Guide)

Pradhan Mantri Vaya Vandana Yojana (PMVVY)

The Pradhan Mantri Vaya Vandana Yojana (PMVVY) is a government-backed pension scheme specifically designed for senior citizens. It offers a guaranteed return and a steady stream of income to provide finence Security in their later years.

1Guaranteed Pension:

The scheme provides a guaranteed pension for 10 years. The interest rate is fixed at the time of investment, which ensures your income is not affected by market fluctuations. For instance, the current interest rate is approximately 7.4% p.a. (as of 2025).

Your Attractive Heading

2Investment Limits:

An individual can invest a maximum amount of ₹15 Lakh in this scheme. This can be investment made in a single lump sum or in multiple installments. The minimum investment amount required to get a pension of ₹1,000 per month is ₹1,56,658.

3 Flexible Pension Payouts:

You can choose to receive your pension monthly, quarterly, half-yearly, or yearly, depending on your needs. For example, if you invest ₹15 Lakh, you can receive a pension of approximately ₹9,250 every month for the entire 10-year period.

4Early Exit and Loan Facility:

The scheme also includes provisions for premature exit in special circumstances, like a critical illness. Additionally, you can avail of a loan against the policy after 3 years of investment. The maximum loan amount is 75% of the purchase price.

5 Return of Purchase Price:

At the end of the 10-year policy term, the original investment amount (purchase price) is returned to the investor. If the policyholder passes away during the term, the purchase price is paid to the nominee.

7How a Systematic Withdrawal Plan (SWP) Works

1. Creating a Regular Income

An SWP allows you to create a regular, fixed income from your existing mutual fund investment. This is often used by retirees or individuals who have a lump sum of money and need a steady cash flow.

2. Your Investment as the Source

The money you receive each month isn’t just interest. It is a combination of your initial investment and the returns it has generated. Essentially, you’re withdrawing a part of your own capital over a period of time.3. Potential for Continued Growth

3. Potential for Continued Growth

Even as you withdraw money, the remaining amount in the mutual fund stays invested. This means it continues to have the potential to grow, which can help your investment last longer and potentially even increase in value over time.

4. An Example with Numbers

For instance, if you have a ₹10 Lakh investment, you could set up an SWP to withdraw ₹5,000 per month. Over the course of a year, you would receive ₹60,000 in income while the remaining ₹9,40,000 continues to grow in the fund.

Senior Citizen Savings Scheme (SCSS) A government-backed, secure plan for senior citizens that provides a fixed, regular income. Post Office Monthly Income Scheme (POMIS) A low-risk option from the Post Office that offers a steady monthly income. Monthly Income Plan (MIP) A type of mutual fund that balances debt and equity investments to provide a regular income with some potential for growth. Fixed Deposits (FDs) A traditional and secure investment where you can choose to receive your interest earnings on a monthly basis. Corporate Bonds You receive regular interest payments by lending money to a corporation through these bonds. Systematic Withdrawal Plan (SWP) Not a scheme, but a way to get a fixed cash flow by setting up regular withdrawals from your existing mutual fund investment.

Call To Action

Click here I am unable to display the response in a box. I can, however, provide a concise response for you. Senior Citizen Savings Scheme (SCSS): Get a secure, fixed income for your retirement. Invest in SCSS today. Post Office Monthly Income Scheme (POMIS): Looking for a safe and steady monthly income? Start your POMIS investment now. Monthly Income Plan (MIP): Want to earn regular income while growing your money? Explore MIPs. Fixed Deposits (FDs): Turn your savings into monthly earnings. Open a Fixed Deposit with a monthly payout option. Corporate Bonds: Diversify your portfolio and earn regular interest. Consider investing in Corporate Bonds. Systematic Withdrawal Plan (SWP): Need a regular cash flow? Set up an SWP from your mutual fund.

FAQ Ideas for Your Article”What is the minimum investment required for these schemes?””Are these schemes taxable?””How do I choose the right scheme for my age and risk tolerance?””Can I withdraw my money before the maturity period ends?””What is the difference between an FD and a POMIS?””How safe are these investments?”

.

What is FAQ?

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

Leave a Comment