Managing money can feel confusing when you are just starting. You may earn money but still wonder where it goes, struggle to save consistently, or feel unsure about budgeting, debt, emergency funds, and investing.

The good news is that personal finance does not have to be complicated. You do not need a high income, advanced financial knowledge, or a perfect plan to begin. You only need to understand your current situation, make a few practical decisions, and build better money habits over time.

This Personal Finance for Beginners guide will help you understand the essential steps needed to take control of your money. You will learn how to track your income and expenses, create a realistic budget, build savings, prepare for emergencies, manage debt, and start investing according to your financial goals.

In this guide, we will break everything down into 10 practical steps. Each step includes clear explanations, realistic examples, and simple actions you can apply in your daily life. Whether you are a student, a beginner, a salaried employee, or someone trying to improve your financial situation, this guide will help you build a stronger financial foundation and create a clear plan for your money in 2026.

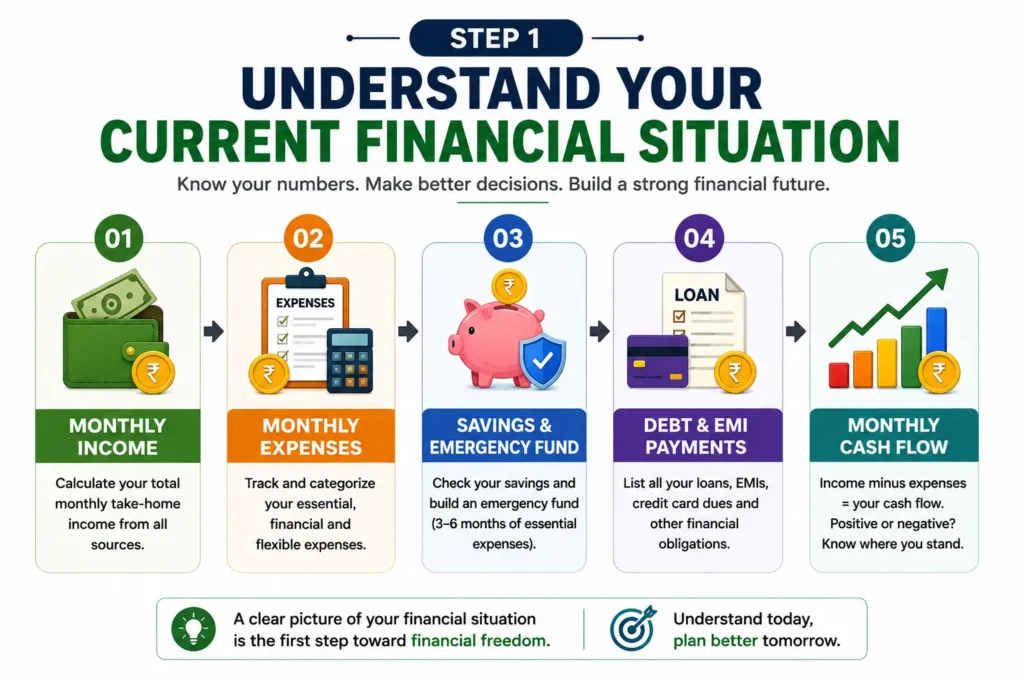

Step 1: Understand Your Current Financial Situation

Before creating a budget, building an emergency fund, paying off debt, or investing, you need to understand where you currently stand with your money. Many people know their monthly salary, but they do not know exactly where that money goes. They may feel that they are always short of money, even when their income seems reasonable.

For personal finance beginners, understanding your current financial situation is the foundation of good money management. You do not need advanced financial knowledge, expensive software, or complicated calculations. A notebook, a spreadsheet, your bank statements, and your UPI transaction history are enough to begin.

Your goal is not to judge yourself or feel guilty about past spending. The goal is to understand your financial reality. Once you know how much you earn, spend, save, and owe, you can create a financial plan that fits your actual life instead of following advice that may not work for your situation.

Start by reviewing these five areas:

- Your monthly income

- Your regular and flexible expenses

- Your savings and emergency money

- Your loans and other debts

- Your monthly cash flow

SEBI explains that documenting income and expenses can help people understand their financial position, control spending, manage debt, save money, and work toward financial goals. You can read its official guide on financial goals and budgeting for additional financial education.

1. Calculate Your Actual Monthly Income

The first step is to calculate the money you actually receive during a normal month. Include your salary, wages, freelance income, business income, commissions, part-time earnings, rental income, or other regular sources.

If you have a fixed job, use your take-home income, not only the salary written in your employment agreement. Take-home income is the amount that actually reaches your bank account after deductions.

For example, if your monthly salary is ₹30,000 but ₹2,000 is deducted before payment, your usable monthly income is ₹28,000. Your budget should be based on ₹28,000 because that is the amount available for expenses, savings, and financial goals.

| Income Source | Monthly Amount |

|---|---|

| Salary | ₹25,000 |

| Part-time work | ₹3,000 |

| Freelance work | ₹2,000 |

| Total Monthly Income | ₹30,000 |

If your income changes every month, do not create your financial plan using your highest-income month. Review your income from the previous three to six months and calculate a realistic average. You can also use your lowest normal monthly income as a safer starting point for essential expenses.

If your earnings are irregular, read our detailed guide on how to budget with an irregular income. It explains how to calculate a minimum income level, prioritize essential expenses, and manage months when earnings are lower.

2. Track Your Monthly Expenses Before Creating a Budget

After calculating your income, review where your money is going. Do not depend only on memory because small expenses are easy to forget. A ₹100 snack, a ₹200 online purchase, or several small UPI payments may not seem important individually, but together they can affect your monthly savings.

Review your bank statements, UPI history, cash spending, and recurring payments. Record what you actually spent—not what you think you should have spent. An honest record gives you a useful starting point for improving your financial habits.

A practical way to organize expenses is to divide them into three groups.

Essential Expenses

- Rent or housing

- Groceries and basic food

- Electricity, phone, and internet bills

- Transport

- Healthcare and medicines

- Education expenses

Financial Commitments

- Loan EMIs

- Credit-card payments

- Insurance premiums

- Other required payments

Flexible Expenses

- Eating out

- Entertainment

- Online shopping

- Subscriptions

- Impulse purchases

- Optional lifestyle spending

You do not have to remove every flexible expense. The purpose of expense tracking is to understand your choices and identify spending that does not provide enough value. A good personal budget should be realistic and sustainable, not so restrictive that you abandon it after a few weeks.

SEBI’s official guide on managing income and expenses also recommends listing income sources, categorizing expenses, tracking spending, and allocating money toward savings and investments.

If you receive a regular salary, our Day 1 to Day 30 salary management plan can help you organize your income after payday and divide money between bills, savings, goals, and personal spending.

3. Calculate Your Monthly Cash Flow

Your monthly cash flow shows whether you are earning more than you spend. It is one of the simplest ways to understand your current financial health.

Monthly Cash Flow = Total Monthly Income − Total Monthly Expenses

| Financial Item | Amount |

|---|---|

| Total monthly income | ₹30,000 |

| Essential expenses | ₹17,000 |

| Loan payments | ₹4,000 |

| Flexible expenses | ₹5,000 |

| Money Remaining | ₹4,000 |

In this example, ₹4,000 remains after all monthly expenses. This amount could be used for savings, an emergency fund, additional debt repayment, investing, or another financial goal.

If your result is negative, it means your expenses are higher than your income. This is not a reason to panic. It is a signal that your current money system needs adjustment. You may need to reduce avoidable expenses, review recurring payments, increase income, or change the order of your financial priorities.

Do not try to fix everything at once. First, identify the largest reason for the negative cash flow. A single change—such as reducing an unnecessary recurring expense—may be more useful than making many small changes that are difficult to maintain.

4. Review Your Savings and Emergency Fund

Next, calculate how much money you have saved and how much is available for unexpected expenses. Include money in your savings account, a separate emergency fund, or another easily accessible account.

Ask yourself:

- How much money can I access quickly if an emergency occurs?

- Could I pay for an urgent medical bill or necessary repair?

- How many months of essential expenses could my savings cover?

- Is my emergency money separate from my everyday spending money?

For example, if your essential monthly expenses are ₹15,000 and you have ₹30,000 in accessible savings, your savings could cover approximately two months of essential expenses.

An emergency fund is generally meant for unexpected costs, such as urgent repairs, medical expenses, or a temporary loss of income. The amount you need depends on your income stability, responsibilities, expenses, and personal situation. The Consumer Financial Protection Bureau’s emergency-fund guide explains why emergency savings can reduce the need to depend on loans or credit when an unexpected expense occurs.

If you are starting from zero, you do not need to save a large amount immediately. You could begin with ₹500 or ₹1,000 per month and increase the amount when your income allows. Small, consistent savings can still create a useful financial cushion over time.

For practical ideas to create more room in your budget, read our guide on how to save money fast in 30 days. It includes realistic strategies for reducing unnecessary spending without making your daily life unnecessarily difficult.

5. List Your Debts and Monthly Payments

If you have a personal loan, education loan, credit-card balance, borrowed money, or another financial obligation, write down the details clearly. Avoiding debt information may temporarily feel easier, but it makes financial planning more difficult.

For each debt, record:

- Total amount remaining

- Interest rate, if known

- Required monthly payment

- Payment due date

- Remaining repayment period

| Debt | Amount Remaining | Monthly Payment |

|---|---|---|

| Personal loan | ₹50,000 | ₹3,000 |

| Credit-card balance | ₹10,000 | ₹1,000 |

Once you can see all your debts in one place, you can compare the balances, interest rates, and payment requirements. Some people prefer paying the smallest debt first to build motivation, while others focus on higher-interest debt to reduce interest costs. The right approach depends on your financial situation and ability to make payments consistently.

Before taking a new loan, understand the total repayment responsibility, interest cost, fees, and repayment period. Borrowing can create long-term pressure if the monthly payment does not fit your income. For additional investor education, SEBI provides guidance on prioritizing needs, wants, and financial priorities.

6. Review Your Financial Habits and Spending Patterns

Your financial numbers show what is happening, but your habits often explain why it is happening. Two people with similar incomes may have very different financial results because their spending, saving, and decision-making habits are different.

Ask yourself:

- Do I check my account balance before spending?

- Do I save at the beginning of the month or only save what is left?

- Do I make unplanned purchases because of discounts or social pressure?

- Do I know how much I spend on subscriptions?

- Do I review my finances regularly?

- Do I compare prices before making a large purchase?

Good financial habits are usually built through small actions repeated over time. You do not need to change everything in one day. For example, reviewing your expenses every Sunday may help you notice problems before they become larger.

Students and young adults can also read our guide on financial habits every college student should develop. Many of these habits can help beginners build a stronger relationship with money before taking bigger financial decisions.

7. Use Financial Tools Carefully

Budgeting apps, expense trackers, banking tools, and AI-powered finance tools can help you organize expenses, monitor spending, set reminders, and understand financial information. However, a tool cannot automatically make the right financial decision for you. It should support your judgment, not replace it.

Before connecting an app to your financial accounts, review its privacy policy, permissions, security practices, and data-sharing rules. Avoid entering sensitive banking information into tools that you do not trust.

To explore useful options, read our guide on the best AI tools to manage personal finances. Choose a tool based on your actual needs instead of downloading many apps that you may never use.

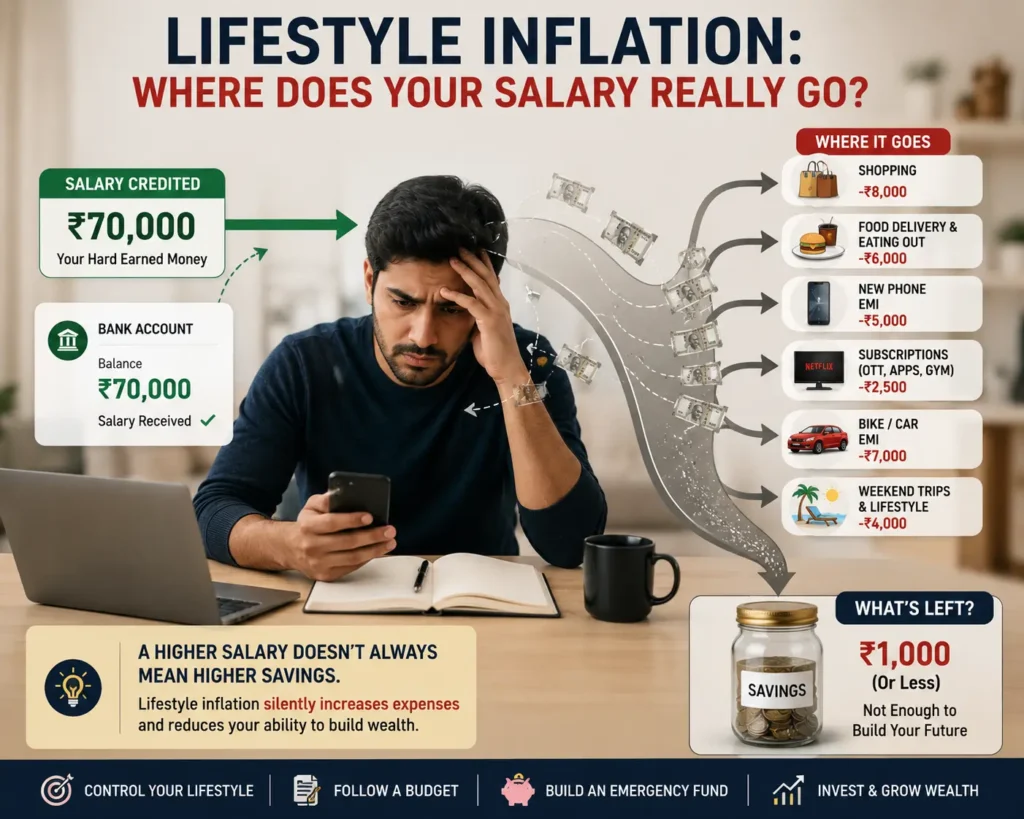

A Simple Real-Life Example

Rahul earns ₹30,000 per month. He believes that he should be able to save ₹8,000, but his bank balance is almost empty before every payday.

After reviewing one month of transactions, Rahul discovers that ₹2,000 goes toward food delivery, ₹1,200 goes toward subscriptions he rarely uses, and ₹1,500 goes toward unplanned online purchases. None of these expenses seemed very large on their own, but together they were reducing his ability to save.

Rahul does not remove every enjoyable expense. Instead, he cancels unused subscriptions, sets a monthly limit for food delivery, and waits 24 hours before making non-essential purchases. These changes improve his monthly cash flow without making his budget too restrictive.

The lesson is simple: you cannot improve a financial problem until you understand what is causing it.

Common Mistake: Trying to Fix Everything at Once

A common mistake among personal finance beginners is trying to cut every expense, repay all debt, save a large amount, and start investing at the same time. This can create an unrealistic plan that is difficult to follow.

Instead, understand your current position first. Then choose one or two improvements that can make the biggest difference. For example, you could cancel one unused subscription, save ₹1,000 automatically, or pay an additional ₹500 toward a high-interest debt.

If you earn a reasonable income but still struggle to save, read our article Why Can’t I Save Money? 5 Hidden Reasons You’re Still Broke Even With a Good Salary. It explains how lifestyle inflation, hidden expenses, and spending patterns can affect savings.

Step 1 Action Plan

- Calculate your actual monthly take-home income.

- Review your bank statements, UPI history, and cash spending.

- Track your expenses for at least 30 days.

- Separate essential expenses from flexible spending.

- Calculate your monthly cash flow.

- Write down your savings and available emergency money.

- List every debt and monthly payment.

- Choose one financial habit to improve this month.

Quick Takeaway

Understanding your income, expenses, savings, debt, financial habits, and monthly cash flow gives you a strong foundation for managing money. You do not need to solve every financial problem today. First, understand your starting point. Once your numbers are clear, you can create realistic goals and build a financial plan that fits your actual situation.

Now that you understand your current financial position, the next step is to create a realistic budget that helps you control spending, protect your priorities, and make steady progress toward your financial goals.

2. Build an Emergency Fund to Protect Your Financial Future

Life does not always follow your monthly budget. A sudden medical bill, phone repair, job loss, family emergency, or unexpected travel expense can create financial pressure without warning. That is why building an emergency fund is one of the most important personal finance tips for beginners in 2026.

An emergency fund is money kept separately for genuine unexpected expenses. It is not money for shopping, entertainment, a planned vacation, or buying something just because it is on sale. Its main purpose is to give you financial breathing room when life becomes expensive unexpectedly.

According to the Consumer Financial Protection Bureau’s emergency fund guide, even a small amount of emergency savings can provide financial security and help people recover from unexpected expenses without immediately depending on credit or loans.

Why an Emergency Fund Matters in Personal Finance

Imagine that Rahul earns ₹25,000 per month. He spends almost all of his income and keeps no money aside. One day, his phone suddenly stops working, and the repair costs ₹6,000. Because Rahul has no emergency savings, he may need to borrow money, use a credit card, or delay another important payment.

Now imagine that Rahul had saved ₹500 every week. After several months, he would have built a useful financial cushion. The repair would still be inconvenient, but it would not automatically turn into debt.

This is the real value of an emergency fund. It may not make you rich, but it can stop a small financial problem from becoming a much larger one.

How Much Should You Keep in an Emergency Fund?

There is no single emergency-fund amount that is perfect for everyone. Your target should depend on your income, monthly essential expenses, job stability, family responsibilities, and how predictable your earnings are.

| Financial Situation | Possible Emergency-Fund Goal |

|---|---|

| Student or beginner with limited income | Start with ₹5,000–₹10,000 |

| Person with a stable monthly salary | Build 1–3 months of essential expenses |

| Freelancer or person with irregular income | Consider 3–6 months of essential expenses |

| Person supporting a family | Build a larger cushion based on responsibilities |

For example, if your essential monthly expenses are ₹15,000, you could first aim for ₹15,000. After reaching that goal, you could gradually work toward ₹30,000 or more. You do not need to build the entire amount in one month.

If your income changes from month to month, your savings plan should also be flexible. You can learn a practical system for handling changing earnings in our guide on how to budget with an irregular income.

Start Small Instead of Waiting for the “Perfect Time”

Many people believe they must earn a high salary before they can start saving. In reality, waiting for the perfect income can delay the habit for years. A small and consistent contribution is often more useful than an ambitious plan that you stop after two weeks.

- Save ₹20 or ₹50 whenever you receive money.

- Set aside ₹100–₹500 every week if your budget allows.

- Save a percentage of extra income, bonuses, or freelance payments.

- Increase your contribution when your income grows.

For example, saving ₹50 per day could build approximately ₹1,500 in one month. Saving ₹500 per week could create around ₹26,000 in one year, before considering any interest. The amount may look small at first, but consistency creates momentum.

If saving feels difficult even when you earn a reasonable income, first identify where your money is quietly disappearing. Our article on why you can’t save money even with a good salary explains hidden spending patterns and practical ways to improve your savings.

Keep Your Emergency Money Separate

Keeping emergency money in the same account you use for daily spending can make it easier to spend accidentally. A separate savings account or another clearly labelled account can help create a mental boundary between everyday money and emergency money.

You could name the account “Emergency Fund” and avoid connecting it to routine shopping payments. The money should remain accessible when a genuine emergency happens, but it should not be so convenient that you spend it on ordinary wants.

Before choosing where to keep your emergency savings, consider three things:

- Safety: The money should not be exposed to unnecessary risk.

- Accessibility: You should be able to access it when a real emergency occurs.

- Stability: The value should not fluctuate heavily when you may need the money soon.

Emergency money is different from long-term investment money. Investments may rise or fall in value, while an emergency fund is designed primarily for financial stability and quick access.

Use Your Emergency Fund Only for Real Emergencies

Before withdrawing money, ask yourself:

“Is this expense unexpected, necessary, and difficult to manage without using my emergency savings?”

A sudden medical expense, urgent home repair, essential vehicle repair, or temporary loss of income may qualify. A planned holiday, new gadget, festival shopping, or a discount offer usually does not.

After using the fund, begin rebuilding it gradually. You do not need to replace the entire amount immediately. Return to your normal saving routine and increase contributions when possible.

A Simple 30-Day Emergency-Fund Action Plan

| Week | Action |

|---|---|

| Week 1 | Calculate your essential monthly expenses. |

| Week 2 | Open or choose a separate place for emergency savings. |

| Week 3 | Save your first amount, even if it is only ₹100 or ₹500. |

| Week 4 | Review your spending and choose a realistic monthly saving amount. |

For a broader step-by-step money system, you can also read our guide on financial planning for beginners. It explains how budgeting, saving, debt management, and long-term goals can work together.

Key Takeaway

Building an emergency fund is not about saving a huge amount overnight. It is about creating a financial safety net one small contribution at a time. Start with a realistic target, keep the money separate, use it only for genuine emergencies, and rebuild it after you use it.

Among the most practical personal finance tips for beginners, this habit can reduce financial stress and help you avoid unnecessary debt when unexpected expenses appear.

Next: Once you have started building a financial safety net, the next step is to understand how to reduce expensive debt without damaging your monthly budget.

Step 3: Pay Off High-Interest Debt and Avoid Unnecessary Borrowing

Debt can help you pay for an important need, such as education, a home, or an emergency. However, debt can become difficult to manage when monthly payments take a large part of your income or when high interest causes the total amount to grow over time.

For personal finance beginners, learning how to manage debt is an important part of building financial stability. The goal is not always to become debt-free overnight. The goal is to understand what you owe, make payments on time, reduce expensive debt strategically, and avoid borrowing for expenses you may not be able to afford.

Before choosing a repayment strategy, create a clear list of every loan, credit-card balance, EMI, or other amount you owe. When all your debt is visible in one place, it becomes easier to decide what to pay first and how much you can realistically contribute each month.

Understand the True Cost of Your Debt

Many people focus only on the monthly EMI. However, the EMI does not always show the complete cost of borrowing. You should also understand the interest rate, repayment period, processing fees, late-payment charges, and total amount you may repay.

For example, two loans may have the same monthly payment but different interest rates or repayment periods. The loan with the higher interest rate may cost more over time, even if the monthly payment appears manageable.

| Debt Type | Amount Remaining | Interest Rate | Minimum Monthly Payment |

|---|---|---|---|

| Credit-card balance | ₹20,000 | 36% per year | ₹2,000 |

| Personal loan | ₹50,000 | 16% per year | ₹3,000 |

| Education loan | ₹1,50,000 | 9% per year | ₹4,000 |

In this example, the credit-card balance has the highest interest rate. If all minimum payments are affordable and current, paying extra toward the highest-interest debt may reduce interest costs. However, your repayment plan should consider your complete financial situation.

Before borrowing, review the repayment responsibility carefully. SEBI’s official guide on thinking before you borrow money explains that borrowing creates financial responsibilities and should not be used for avoidable or unnecessary expenses.

Create a Complete Debt List

Write down every debt in one place. Do not rely only on memory because it is easy to forget due dates, fees, or small balances.

Your debt list should include:

- The name of the lender

- The total amount remaining

- The interest rate

- The minimum monthly payment

- The payment due date

- The remaining repayment period

- Any late-payment fees or penalties

Once your list is complete, calculate the total amount you pay toward debt every month. Compare that number with your monthly take-home income and essential expenses.

If you have not created a clear monthly spending plan yet, review Step 2: Create a Realistic Budget before increasing your debt payments. A repayment plan should fit your budget so that you can continue paying consistently.

Choose a Debt-Repayment Method

Two popular debt-repayment methods are the debt avalanche and the debt snowball. Both can work, but they focus on different priorities.

Method 1: The Debt Avalanche

With the debt avalanche method, you continue making the required minimum payments on all debts. Any extra money is directed toward the debt with the highest interest rate.

After the highest-interest debt is paid off, you move the extra payment to the debt with the next-highest interest rate.

This method may reduce the total interest you pay over time. The Consumer Financial Protection Bureau’s debt-reduction guide describes the highest-interest-rate method as one of the main approaches people can use to reduce debt.

Method 2: The Debt Snowball

With the debt snowball method, you continue making the required payments on all debts and direct extra money toward the smallest balance first.

After paying off the smallest debt, you add that payment amount to the next-smallest debt. This creates a series of small wins that may help some people stay motivated.

The debt snowball may not always minimize total interest, but motivation can be valuable if it helps you continue the repayment plan.

| Method | Priority | Possible Benefit |

|---|---|---|

| Debt avalanche | Highest interest rate first | May reduce total interest costs |

| Debt snowball | Smallest balance first | May create faster motivational wins |

Choose the method that you can follow consistently. A mathematically efficient plan is less useful if it is too difficult to maintain.

Always Pay Required Amounts on Time

Even when you are focusing extra money on one debt, continue making the required payments on your other debts. Missing payments may result in late fees, additional interest, or other financial consequences.

Set reminders a few days before each due date. If your income arrives on a predictable schedule, you may also consider automatic payments, provided you keep enough money in your account.

RBI’s Financial Literacy Guide includes responsible borrowing and timely repayment as important financial education topics.

Do Not Borrow More While Paying Off Existing Debt

It is difficult to reduce debt if new borrowing continues to replace the amount you repay. Before taking another loan or using credit for a non-essential purchase, ask yourself:

- Is this expense necessary?

- Can I wait and save for it instead?

- Can I afford the monthly payment after paying essential expenses?

- What will the total borrowing cost be?

- Will this new payment make my current debt harder to manage?

A new loan may be appropriate for some important needs, but it should not be treated as free money. Every borrowed amount has a repayment responsibility.

SEBI also advises investors not to borrow money for securities-market investments. You can review its official investment dos and don’ts before making investment decisions.

Use Extra Income Strategically

If you receive a bonus, freelance payment, tax refund, or other extra income, you do not have to use all of it for debt. However, allocating a planned portion toward high-interest debt may help you reduce the balance faster.

For example, imagine that you receive an extra ₹10,000:

| Purpose | Amount |

|---|---|

| Emergency savings | ₹3,000 |

| Extra high-interest debt payment | ₹5,000 |

| Upcoming essential expense | ₹2,000 |

This is only an example. If you have no emergency savings, keeping some money available may help you avoid borrowing again when an unexpected expense occurs.

For ideas on finding extra money in your monthly budget, read our guide on how to save money fast in 30 days.

A Real-Life Debt Example

Arman has three debts: a ₹5,000 credit-card balance, a ₹20,000 personal loan, and a ₹40,000 education loan. He pays the required amount on each debt but has an additional ₹2,000 available every month.

Using the debt avalanche method, Arman directs the extra ₹2,000 toward the debt with the highest interest rate while continuing the required payments on the other two debts. When the first debt is paid off, he adds its previous payment to the next priority.

Using the debt snowball method, he would pay the smallest balance first. Both approaches can create progress. The important part is that Arman has a clear plan and avoids adding unnecessary new debt.

Common Debt-Management Mistakes to Avoid

- Looking only at the EMI and ignoring the interest rate

- Taking a new loan to pay for avoidable expenses

- Missing due dates because payments are not tracked

- Paying extra toward one debt while missing required payments on another

- Using new credit while trying to reduce existing debt

- Ignoring fees, penalties, and the total repayment cost

- Borrowing money to make high-risk investments

Step 3 Debt-Repayment Action Plan

- List every debt, balance, interest rate, and due date.

- Calculate your total required monthly debt payments.

- Make a realistic budget before increasing repayments.

- Choose the debt avalanche or debt snowball method.

- Continue making required payments on all debts.

- Direct extra money toward your chosen priority debt.

- Avoid unnecessary new borrowing.

- Review your progress once each month.

Quick Takeaway

Managing debt is not only about paying money faster. It is about understanding interest costs, making payments on time, choosing a realistic strategy, and avoiding unnecessary borrowing.

For personal finance beginners, a clear debt plan can reduce financial pressure and create more room for savings and future goals. Progress may be gradual, but consistent payments and better borrowing decisions can make a meaningful difference over time.

Now that you have started protecting yourself with savings and managing expensive debt, the next step is to automate your savings and build consistent financial habits.

Step 3: Pay Off High-Interest Debt and Avoid Unnecessary Borrowing

Debt can help you pay for an important need, such as education, a home, or an emergency. However, debt can become difficult to manage when monthly payments take a large part of your income or when high interest causes the total amount to grow over time.

For personal finance beginners, learning how to manage debt is an important part of building financial stability. The goal is not always to become debt-free overnight. The goal is to understand what you owe, make payments on time, reduce expensive debt strategically, and avoid borrowing for expenses you may not be able to afford.

Before choosing a repayment strategy, create a clear list of every loan, credit-card balance, EMI, or other amount you owe. When all your debt is visible in one place, it becomes easier to decide what to pay first and how much you can realistically contribute each month.

Understand the True Cost of Your Debt

Many people focus only on the monthly EMI. However, the EMI does not always show the complete cost of borrowing. You should also understand the interest rate, repayment period, processing fees, late-payment charges, and total amount you may repay.

For example, two loans may have the same monthly payment but different interest rates or repayment periods. The loan with the higher interest rate may cost more over time, even if the monthly payment appears manageable.

| Debt Type | Amount Remaining | Interest Rate | Minimum Monthly Payment |

|---|---|---|---|

| Credit-card balance | ₹20,000 | 36% per year | ₹2,000 |

| Personal loan | ₹50,000 | 16% per year | ₹3,000 |

| Education loan | ₹1,50,000 | 9% per year | ₹4,000 |

In this example, the credit-card balance has the highest interest rate. If all minimum payments are affordable and current, paying extra toward the highest-interest debt may reduce interest costs. However, your repayment plan should consider your complete financial situation.

Before borrowing, review the repayment responsibility carefully. SEBI’s official guide on thinking before you borrow money explains that borrowing creates financial responsibilities and should not be used for avoidable or unnecessary expenses.

Create a Complete Debt List

Write down every debt in one place. Do not rely only on memory because it is easy to forget due dates, fees, or small balances.

Your debt list should include:

- The name of the lender

- The total amount remaining

- The interest rate

- The minimum monthly payment

- The payment due date

- The remaining repayment period

- Any late-payment fees or penalties

Once your list is complete, calculate the total amount you pay toward debt every month. Compare that number with your monthly take-home income and essential expenses.

If you have not created a clear monthly spending plan yet, review Step 2: Create a Realistic Budget before increasing your debt payments. A repayment plan should fit your budget so that you can continue paying consistently.

Choose a Debt-Repayment Method

Two popular debt-repayment methods are the debt avalanche and the debt snowball. Both can work, but they focus on different priorities.

Method 1: The Debt Avalanche

With the debt avalanche method, you continue making the required minimum payments on all debts. Any extra money is directed toward the debt with the highest interest rate.

After the highest-interest debt is paid off, you move the extra payment to the debt with the next-highest interest rate.

This method may reduce the total interest you pay over time. The Consumer Financial Protection Bureau’s debt-reduction guide describes the highest-interest-rate method as one of the main approaches people can use to reduce debt.

Method 2: The Debt Snowball

With the debt snowball method, you continue making the required payments on all debts and direct extra money toward the smallest balance first.

After paying off the smallest debt, you add that payment amount to the next-smallest debt. This creates a series of small wins that may help some people stay motivated.

The debt snowball may not always minimize total interest, but motivation can be valuable if it helps you continue the repayment plan.

| Method | Priority | Possible Benefit |

|---|---|---|

| Debt avalanche | Highest interest rate first | May reduce total interest costs |

| Debt snowball | Smallest balance first | May create faster motivational wins |

Choose the method that you can follow consistently. A mathematically efficient plan is less useful if it is too difficult to maintain.

Always Pay Required Amounts on Time

Even when you are focusing extra money on one debt, continue making the required payments on your other debts. Missing payments may result in late fees, additional interest, or other financial consequences.

Set reminders a few days before each due date. If your income arrives on a predictable schedule, you may also consider automatic payments, provided you keep enough money in your account.

RBI’s Financial Literacy Guide includes responsible borrowing and timely repayment as important financial education topics.

Do Not Borrow More While Paying Off Existing Debt

It is difficult to reduce debt if new borrowing continues to replace the amount you repay. Before taking another loan or using credit for a non-essential purchase, ask yourself:

- Is this expense necessary?

- Can I wait and save for it instead?

- Can I afford the monthly payment after paying essential expenses?

- What will the total borrowing cost be?

- Will this new payment make my current debt harder to manage?

A new loan may be appropriate for some important needs, but it should not be treated as free money. Every borrowed amount has a repayment responsibility.

SEBI also advises investors not to borrow money for securities-market investments. You can review its official investment dos and don’ts before making investment decisions.

Use Extra Income Strategically

If you receive a bonus, freelance payment, tax refund, or other extra income, you do not have to use all of it for debt. However, allocating a planned portion toward high-interest debt may help you reduce the balance faster.

For example, imagine that you receive an extra ₹10,000:

| Purpose | Amount |

|---|---|

| Emergency savings | ₹3,000 |

| Extra high-interest debt payment | ₹5,000 |

| Upcoming essential expense | ₹2,000 |

This is only an example. If you have no emergency savings, keeping some money available may help you avoid borrowing again when an unexpected expense occurs.

For ideas on finding extra money in your monthly budget, read our guide on how to save money fast in 30 days.

A Real-Life Debt Example

Arman has three debts: a ₹5,000 credit-card balance, a ₹20,000 personal loan, and a ₹40,000 education loan. He pays the required amount on each debt but has an additional ₹2,000 available every month.

Using the debt avalanche method, Arman directs the extra ₹2,000 toward the debt with the highest interest rate while continuing the required payments on the other two debts. When the first debt is paid off, he adds its previous payment to the next priority.

Using the debt snowball method, he would pay the smallest balance first. Both approaches can create progress. The important part is that Arman has a clear plan and avoids adding unnecessary new debt.

Common Debt-Management Mistakes to Avoid

- Looking only at the EMI and ignoring the interest rate

- Taking a new loan to pay for avoidable expenses

- Missing due dates because payments are not tracked

- Paying extra toward one debt while missing required payments on another

- Using new credit while trying to reduce existing debt

- Ignoring fees, penalties, and the total repayment cost

- Borrowing money to make high-risk investments

Step 3 Debt-Repayment Action Plan

- List every debt, balance, interest rate, and due date.

- Calculate your total required monthly debt payments.

- Make a realistic budget before increasing repayments.

- Choose the debt avalanche or debt snowball method.

- Continue making required payments on all debts.

- Direct extra money toward your chosen priority debt.

- Avoid unnecessary new borrowing.

- Review your progress once each month.

Quick Takeaway

Managing debt is not only about paying money faster. It is about understanding interest costs, making payments on time, choosing a realistic strategy, and avoiding unnecessary borrowing.

For personal finance beginners, a clear debt plan can reduce financial pressure and create more room for savings and future goals. Progress may be gradual, but consistent payments and better borrowing decisions can make a meaningful difference over time.

Now that you have started protecting yourself with savings and managing expensive debt, the next step is to automate your savings and build consistent financial habits.

Step 4: Automate Your Savings and Investments for Consistent Growth

Creating a budget and building an emergency fund are important, but consistency is what turns good financial intentions into long-term progress. Many people plan to save money every month, yet they wait until the end of the month and discover that very little is left. Automating your money can help solve this problem.

For personal finance beginners, automation means setting up a planned transfer so that a portion of your income moves toward savings or investments automatically. Instead of depending only on memory, motivation, or willpower, you create a system that supports your financial goals every time you receive money.

Automation does not guarantee investment returns, and it does not replace financial planning. However, it can make saving more consistent and reduce the temptation to spend money that was intended for your future.

What Does Automating Your Finances Mean?

Financial automation means using your bank, investment platform, or payment system to complete selected money tasks automatically on a fixed date.

For example, if you receive your salary on the 5th of every month, you could arrange:

- ₹1,000 to move into your emergency savings account on the 6th

- ₹2,000 to be invested through a planned investment contribution on the 7th

- Your regular EMI or bill payment to be scheduled before its due date

This approach follows a simple principle: save first and spend the remaining amount according to your budget. It is often easier than trying to save whatever remains after a month of spending.

Why Automation Can Improve Your Money Habits

People are busy, and financial tasks are easy to postpone. You may tell yourself that you will transfer money tomorrow, but an unexpected expense or an attractive purchase can change the plan.

Automation reduces the number of decisions you need to make each month. Once the system is set up correctly, your planned contribution can happen without requiring repeated effort.

| Manual Saving | Automated Saving |

|---|---|

| You must remember to transfer money | The transfer follows a scheduled date |

| Saving may be delayed | Saving can happen soon after income arrives |

| Spending may happen before saving | Money is assigned to goals earlier |

| Progress may depend heavily on motivation | A system supports consistency |

Automation is useful because it creates a repeatable process. However, you should still review your account balance and financial plan regularly. An automatic payment is helpful only when the amount and timing are appropriate for your income.

Start With a Small Automatic Savings Amount

You do not need to automate a large amount immediately. Start with an amount that fits your current budget and does not make it difficult to pay essential expenses.

For example, if your monthly income is ₹20,000, your first automated plan could look like this:

| Financial Purpose | Monthly Amount | Transfer Date |

|---|---|---|

| Emergency fund | ₹1,000 | One day after income arrives |

| Long-term investment | ₹2,000 | Two days after income arrives |

| Future annual expenses | ₹500 | One day after income arrives |

In this example, ₹3,500 is assigned to future goals. The remaining income can then be used for essential expenses, debt payments, and personal spending according to the budget.

If ₹3,500 is not affordable, start with ₹500 or ₹1,000. The purpose is to build a sustainable habit. You can increase the amount after reviewing your income and expenses.

Automate Savings Before Automating Investments

If you have no emergency savings and your financial situation is unstable, building a basic emergency fund may be more important than increasing investment contributions. Investment values can rise or fall, while emergency money is intended to remain available for unexpected essential expenses.

A practical order may be:

- Pay essential bills and required debt payments.

- Build a basic emergency fund.

- Automate regular savings.

- Begin long-term investing according to your goals and risk tolerance.

- Increase contributions gradually as your financial position improves.

For a complete beginner-friendly system, you can connect this section with your article on financial planning for beginners.

How Automatic Investment Contributions Work

In India, many investors use a Systematic Investment Plan, commonly called a SIP, to invest a fixed amount at regular intervals in a mutual fund. A SIP is a method of investing regularly; it does not guarantee profits or protect against market losses.

According to the Association of Mutual Funds in India (AMFI), a SIP allows investors to invest a fixed amount periodically. Before investing, understand the fund’s objective, risk level, costs, and whether it matches your financial goals.

For example, someone may invest ₹2,000 per month through a SIP for a long-term goal. The investment amount remains fixed, but the value of the investment can move up or down depending on market performance.

If you are new to mutual funds, your article on best-performing FlexiCap funds can be linked here only if that is the exact working URL. Otherwise, search for the article inside WordPress and select the correct page before publishing.

Choose the Right Date for Automatic Transfers

The timing of automation matters. Setting a transfer date before your income arrives may cause a failed transaction or create pressure on your account balance.

A simple approach is to schedule savings one or two days after your salary, business income, or regular payment usually arrives.

For example:

- Income arrives: 5th of the month

- Emergency-fund transfer: 6th

- Investment contribution: 7th

- Bill and EMI payments: According to their due dates

- Budget review: Last day of the month

If your income is irregular, avoid setting an automatic amount that could leave you short of money. You may prefer to transfer a percentage of each payment manually or automate a small base amount.

A Simple Automation Example

Meera earns ₹30,000 per month. She wants to save and invest but usually spends most of her money before the month ends.

She creates the following system:

| Purpose | Amount |

|---|---|

| Emergency savings | ₹2,000 |

| Long-term investment | ₹3,000 |

| Future expenses | ₹1,000 |

Every month, ₹6,000 is assigned automatically after she receives her income. She then manages the remaining ₹24,000 using her monthly budget.

After three months, Meera reviews the plan. Because her essential expenses are under control, she increases her savings contribution by ₹500. She does not make a large change all at once; she improves the system gradually.

Review Automated Payments Regularly

Automation should not become “set it and forget it.” Your income, expenses, goals, and financial responsibilities may change.

Review your automated transfers at least every three to six months and ask:

- Is the savings amount still affordable?

- Have my essential expenses increased?

- Is my emergency fund progressing toward its target?

- Does my investment still match my financial goal and risk tolerance?

- Have any automatic payments become unnecessary?

- Is there enough money in my account before each payment date?

The SEBI Investor Education portal provides educational information about investing and investor awareness. Before investing, understand the product instead of choosing it only because it is popular or has performed well recently.

Common Automation Mistakes to Avoid

- Automating an amount that is too large for your budget

- Scheduling transfers before income usually arrives

- Ignoring account balances and payment failures

- Investing emergency money in volatile assets

- Increasing investment contributions while high-interest debt remains unmanaged

- Choosing an investment without understanding its risks

- Never reviewing old automatic payments or subscriptions

Step 4: 15-Minute Automation Action Plan

- Review your monthly income and essential expenses.

- Choose a realistic savings amount.

- Select a separate account for emergency savings.

- Schedule the transfer one or two days after income arrives.

- Decide whether you are financially ready for long-term investing.

- Set up investment contributions only after understanding the risks and product.

- Turn on transaction alerts and check that payments are successful.

- Review the entire system every three to six months.

Key Takeaway

Automating savings and investments can make financial progress more consistent because it turns a good intention into a repeatable system. Start with an affordable amount, protect your emergency savings, understand investment risks, and review your automatic payments regularly.

For personal finance beginners, the goal is not to automate the largest possible amount. The goal is to create a sustainable financial system that supports your needs today while helping you prepare for future goals.

Next: After creating a consistent savings system, the next step is to diversify your investments and manage risk instead of depending too heavily on a single asset or investment.

Step 5: Diversify Your Investments and Manage Risk Wisely

After building an emergency fund, managing expensive debt, and creating a regular saving habit, you may begin thinking about long-term investing. However, investing all your money in one company, one sector, one fund, or one type of asset can create unnecessary risk.

For personal finance beginners, diversification means spreading your investments instead of depending too heavily on a single investment. Diversification cannot guarantee profits or prevent all losses, but it may reduce the damage if one investment performs poorly.

A strong investment plan is not only about finding the investment with the highest recent return. It should also consider your financial goals, time horizon, risk tolerance, emergency savings, existing debt, and the purpose of the money you are investing.

What Does Investment Diversification Mean?

Diversification is often explained with the phrase, “Do not put all your eggs in one basket.” In personal finance, this means avoiding excessive dependence on one company, industry, asset class, or investment idea.

For example, imagine that Ravi invests his entire ₹1,00,000 in shares of only one company. If that company faces financial problems, the value of a large part of his investment may fall.

Now imagine that another investor spreads money across different investments based on their goals and risk capacity. If one investment performs poorly, the other investments may reduce the overall impact. This does not remove risk, but it can reduce concentration risk.

| Highly Concentrated Portfolio | More Diversified Portfolio |

|---|---|

| Most money is invested in one company or asset | Money is spread across multiple investments |

| One poor investment may have a large impact | The effect of one investment may be reduced |

| Higher concentration risk | Risk may be spread across different areas |

| Returns depend heavily on one outcome | The portfolio is less dependent on one investment |

The Investor.gov guide to diversification explains that diversification involves spreading investments among different assets to reduce the impact of a single investment on an overall portfolio.

Understand the Main Types of Investment Risk

Investment risk is not only the possibility that prices may fall. Different investments can involve different risks, and understanding them can help you make more informed decisions.

- Market risk: Investment values may rise or fall because of economic conditions, interest rates, company performance, or market sentiment.

- Concentration risk: Too much money is invested in one company, sector, asset, or investment theme.

- Liquidity risk: You may not be able to access your money quickly without selling at an unfavorable price.

- Inflation risk: Your money may lose purchasing power if its growth does not keep up with rising prices.

- Credit risk: A borrower or issuer may fail to make expected payments.

Understanding these risks does not mean avoiding every investment. It means knowing what could happen before you commit your money.

Match Your Investments With Your Financial Goals

Before choosing an investment, decide what the money is for and when you may need it. Money needed next year may require a different approach from money intended for a goal that is ten or twenty years away.

| Financial Goal | Possible Time Horizon | Important Consideration |

|---|---|---|

| Emergency expense | Any time | Safety and quick access may be more important than growth |

| Course fee or planned purchase | 1–2 years | Avoid taking unnecessary market risk with money needed soon |

| Buying a home | 5–10 years | Consider the target date and your ability to handle investment changes |

| Long-term financial independence | 10+ years | Long-term growth, risk, and diversification may become more relevant |

Emergency savings should remain separate from long-term investments because you may need emergency money quickly. If you have not built an emergency fund yet, return to Step 2: Build an Emergency Fund and create a basic financial safety net first.

For a broader money-management framework, you can also read our guide on Financial Planning for Beginners: 10 Simple Steps. It explains how budgeting, saving, debt management, financial goals, and investing can work together.

Understand Asset Allocation

Asset allocation means deciding how your investment money is divided among different investment categories. There is no single allocation that is suitable for everyone.

Your financial goals, income, responsibilities, time horizon, and ability to handle losses can affect the type of allocation that may be appropriate for you.

For educational purposes, a sample portfolio could look like this:

| Investment Category | Example Allocation | Possible Purpose |

|---|---|---|

| Equity-oriented investments | 50% | Long-term growth potential |

| Debt or fixed-income investments | 30% | Potential stability and income |

| Cash or short-term savings | 20% | Liquidity and near-term needs |

This is only an example for understanding asset allocation. It is not a recommended portfolio. Your own allocation should be based on your financial goals, risk capacity, and time horizon.

Diversification Does Not Mean Buying Everything

Some beginners believe that buying many investments automatically creates diversification. However, owning a large number of products does not always reduce risk.

For example, buying shares of ten companies from the same industry may still create concentration risk. Similarly, investing in several funds that hold many of the same companies may create more overlap than you expect.

Before adding a new investment, ask:

- What does this investment add to my portfolio?

- Does it hold many of the same assets I already own?

- Does it support one of my financial goals?

- Do I understand its risks and costs?

- Am I buying it because of a clear plan or only because it recently performed well?

The goal is not to own the largest number of investments. The goal is to avoid unnecessary concentration while keeping your financial plan understandable.

Understand Mutual Funds Before Investing

Mutual funds may provide exposure to multiple securities through a single investment product. However, different funds have different objectives, risks, costs, investment styles, and portfolio holdings.

Before investing, read the scheme information, understand the investment objective, review the risk level, and check whether the fund matches your financial goal.

The AMFI Investor Knowledge Centre provides educational information about mutual funds, investor awareness, and important investment concepts.

If you want to learn more about one mutual-fund category, read our detailed guide on Best Performing FlexiCap Funds. The article can help you understand what to examine beyond past returns, including investment strategy, risk, consistency, and long-term suitability.

A Practical Diversification Example

Suppose Sana has ₹1,20,000 available. Before investing, she checks whether she has enough emergency savings, whether she has expensive debt, and when she may need the money.

She realizes that she may need ₹20,000 within the next year and wants to keep ₹30,000 available for emergencies. Instead of investing the entire ₹1,20,000 in one company, she separates the money according to its purpose.

| Financial Purpose | Example Amount |

|---|---|

| Emergency savings | ₹30,000 |

| Near-term planned expense | ₹20,000 |

| Long-term investment goal | ₹70,000 |

This example shows that diversification is not only about dividing investments. It also includes separating emergency money, short-term goal money, and long-term investment money.

Review Your Investments Without Reacting Emotionally

Investment prices may change every day. Checking your portfolio constantly can increase stress and may encourage emotional decisions.

Instead, review your investments on a planned schedule, such as every six or twelve months, or when your financial goals change.

During a review, ask:

- Does this investment still support my financial goal?

- Has my time horizon changed?

- Has my income or financial responsibility changed?

- Has one investment become too large a part of my portfolio?

- Do I understand what I own?

- Are the risks and costs still acceptable?

A review does not always mean buying or selling. Sometimes the correct action is to continue following a suitable long-term plan.

Use Reliable Investment Information

Investment decisions should not be based only on social-media trends, advertisements, or promises of guaranteed returns. Check official information and understand the product before investing.

The SEBI Investor Education portal provides investor-awareness information and educational resources. It can help beginners understand important investment concepts and recognize the need for informed decision-making.

If you are using digital tools to organize your financial information, read our guide on 10 Best AI Tools to Manage Your Personal Finances in 2026. These tools may help with budgeting, expense tracking, planning, and research, but important financial information should always be verified.

Common Diversification Mistakes to Avoid

- Investing all your money in one company or sector

- Choosing investments only because of recent high returns

- Copying another person’s portfolio without understanding it

- Investing emergency money in volatile assets

- Buying many funds without checking portfolio overlap

- Ignoring investment costs and risk information

- Making decisions because of short-term market fear or excitement

- Assuming diversification guarantees profit or eliminates all losses

Step 5: Investment Diversification Action Plan

- Write down your financial goals and target dates.

- Keep emergency savings separate from long-term investments.

- Review your current investments and identify concentration risk.

- Check whether multiple investments hold similar assets.

- Understand the purpose, risk, and cost of every investment.

- Choose an allocation based on your goals and risk capacity.

- Avoid investing only because of recent returns or online trends.

- Review your portfolio periodically instead of reacting to daily price changes.

Key Takeaway

Diversification is a risk-management strategy, not a guarantee of profit. By spreading investments thoughtfully, matching them with your financial goals, and avoiding excessive dependence on one asset, you can build a more balanced financial plan.

For personal finance beginners, the most important rule is to understand what you own and why you own it. Keep emergency money separate, invest according to your time horizon, and avoid making decisions based only on recent performance.

Next: After building a diversified investment approach, the next step is to improve your financial knowledge and stay informed without becoming overwhelmed by financial news, trends, or social-media advice.

Step 6: Improve Your Financial Knowledge and Stay Informed

Managing money is not only about earning, budgeting, saving, or investing. Good financial decisions also depend on understanding how money works. Financial products, interest rates, investment options, technology, and economic conditions can change over time. That is why improving your financial knowledge can help you make more informed decisions and avoid costly mistakes.

For personal finance beginners, financial education does not mean becoming an accountant, economist, or investment expert. It means learning enough to understand your financial choices, compare options, recognize risks, ask useful questions, and avoid making decisions only because something is popular on social media.

You do not need to study finance for several hours every day. Even 20 to 30 minutes of focused learning each week can improve your understanding when you apply what you learn to your own income, expenses, savings, debt, investments, and financial goals.

Why Financial Knowledge Is Important

Many financial problems happen because people do not fully understand interest rates, loan terms, investment risks, fees, inflation, or the long-term effect of their decisions.

For example, imagine that two people want to invest ₹2,000 every month. The first person invests because a social-media creator says that a particular investment will provide very high returns. The second person spends time learning about risk, diversification, investment time horizons, fees, and how the investment actually works.

Neither person can predict future returns. However, the second person is more likely to understand the possible benefits and risks before investing.

The Consumer Financial Protection Bureau’s financial well-being resources explain that financial well-being includes managing day-to-day finances, handling financial shocks, working toward goals, and having greater freedom to make financial choices.

Learn the Most Important Personal Finance Topics First

There is a huge amount of financial information online. Trying to learn everything at once can create confusion. A better approach is to begin with the topics that directly affect your financial life.

| Financial Topic | What You Should Learn | Why It Matters |

|---|---|---|

| Budgeting | Income, expenses, spending limits, and monthly planning | Helps you understand where your money goes |

| Saving | Emergency funds, savings goals, and consistent saving habits | Helps create financial security |

| Debt | Interest rates, EMIs, repayment periods, and borrowing costs | Helps you manage debt responsibly |

| Investing | Risk, return, diversification, time horizon, and fees | Helps you make informed long-term decisions |

| Financial Goals | Target amounts, deadlines, and monthly contributions | Gives your money a clear purpose |

| Credit | Payment history and responsible borrowing | Can affect future borrowing opportunities |

Start with the topic that is most important to your current situation. If you are struggling to save money, first learn about spending habits and budgeting. If you have expensive debt, understand interest costs and repayment strategies before focusing heavily on investing.

If you earn regularly but still struggle to save, read our detailed guide on why you can’t save money even with a good salary. It explains hidden spending patterns and practical ways to improve your saving habits.

Use Reliable Financial Sources Instead of Following Every Trend

Social media can help you discover financial ideas, but short videos and viral posts often leave out important details. A person may show high investment returns without explaining the risks, fees, losses, taxes, or time involved.

Before acting on financial information, check whether the source is reliable and whether the information applies to your situation.

Ask these questions:

- Who published this information?

- Is the source a government agency, financial regulator, recognized institution, or qualified professional?

- Does the content explain risks as well as possible benefits?

- Is the information current?

- Is someone trying to sell a financial product?

- Can the information be verified through another reliable source?

For beginner investment education, Investor.gov’s introduction to investing explains important topics such as financial goals, risk, diversification, long-term investing, and the difference between saving and investing.

Use Financial Technology to Learn and Manage Money

Technology can make financial learning easier. Budgeting apps, expense trackers, calculators, banking tools, and AI-powered financial tools can help you organize information and understand your financial habits.

However, a tool should support your decisions rather than replace your judgment. Before sharing financial information with an app or AI tool, check its privacy policy, security practices, and the type of information it collects.

To explore useful tools in more detail, read our guide on 10 Best AI Tools to Manage Your Personal Finances in 2026. The article explains how different tools may help with budgeting, expense tracking, financial planning, and money management.

Financial tools can help you organize information, but they may not understand your complete financial situation. Verify important information before making a major financial decision.

Understand an Investment Before You Put Money Into It

One of the most useful financial habits is refusing to invest in something you do not understand. A product may have a professional-looking website, a popular name, or strong past returns, but those factors do not automatically make it suitable for your goals.

Before investing, try to answer these questions in simple language:

- What does this investment actually do?

- How can it make or lose money?

- What are its main risks?

- How long may I need to keep my money invested?

- Can I access the money quickly if necessary?

- What fees or charges may apply?

- Does this investment match my financial goal and risk tolerance?

The Investor.gov guide to investment options explains that different investments have different risks, potential returns, and characteristics. Understanding these factors can help investors make more informed decisions.

If you want to understand one mutual-fund category in greater detail, read our guide on Best Performing FlexiCap Funds. It explains important factors to evaluate beyond past returns, including investment strategy, risk, consistency, and long-term suitability.

Create a Simple Weekly Financial Learning Routine

You do not need a complicated study plan. A small routine is easier to follow and becomes more valuable when you apply the lessons to your own finances.

| Day | Learning Activity | Suggested Time |

|---|---|---|

| Monday | Read one reliable article about budgeting or saving | 10 minutes |

| Wednesday | Learn one financial term, such as inflation or interest | 10 minutes |

| Friday | Study one investment concept or financial risk | 15 minutes |

| Sunday | Apply one lesson to your own financial plan | 15 minutes |

The most important part is application. Reading about budgeting is useful, but reviewing your own spending is more practical. Learning about emergency funds is useful, but saving your first ₹100 or ₹500 turns knowledge into action.

Keep a Personal Finance Learning Notebook

Create a notebook, document, or digital note where you explain financial concepts in your own words. Avoid copying complicated definitions without understanding them.

| Financial Concept | Simple Meaning | Personal Action |

|---|---|---|

| Emergency Fund | Money reserved for unexpected essential expenses | I will begin by saving ₹5,000 |

| Interest Rate | The cost of borrowing or the return offered by some savings products | I will compare rates before borrowing |

| Diversification | Spreading investments to reduce dependence on one investment | I will avoid putting all my money into one company |

Writing financial ideas in your own words can help you identify what you understand and what you need to learn further.

Learn From Your Own Financial Decisions

Your monthly financial activity is also a learning opportunity. At the end of each month, review your decisions and look for useful patterns.

Ask yourself:

- Where did I spend more than expected?

- Did I save the amount I planned?

- Did I borrow money? If yes, why?

- Which expense gave me real value?

- Which expense could I reduce next month?

- Did I make a financial decision without enough information?

For example, suppose you planned to spend ₹3,000 on food but spent ₹4,500. Instead of only saying that your budget failed, find the reason. Did prices increase? Did you order food more often? Did you forget to include an important expense?

The answer can help you create a more realistic financial plan next month.

A Practical Financial Learning Example

Arif wants to invest ₹3,000 every month. Before investing, he spends one week learning about risk, diversification, investment time horizons, and fees.

He discovers that he may need part of the money within one year. Instead of investing the complete ₹3,000 without a plan, he separates his short-term needs from his long-term goals.

| Financial Purpose | Monthly Amount |

|---|---|

| Short-term savings goal | ₹1,000 |

| Emergency savings | ₹1,000 |

| Long-term investment goal | ₹1,000 |

The amounts are only examples. The important lesson is that financial knowledge helped Arif create a plan based on his own needs instead of copying someone else’s investment decision.

Common Financial Learning Mistakes to Avoid

- Believing every viral financial video

- Following investment tips without checking the source

- Focusing only on returns and ignoring risk

- Learning advanced investing before understanding budgeting

- Buying a financial product without reading important information

- Assuming past performance guarantees future results

- Copying another person’s financial plan without considering your own goals

- Reading financial content without applying anything to your own situation

Step 6: Financial Learning Action Plan

- Choose one personal finance topic to study this week.

- Use an official or reliable educational source.

- Learn the concept in simple language.

- Write the main lesson in your own words.

- Check how the concept applies to your income, expenses, savings, or goals.

- Take one small action based on what you learned.

- Review the result at the end of the month.

- Continue learning without rushing into financial products.

Key Takeaway

Financial knowledge is not about memorizing complicated terms. It is about understanding how your money decisions affect your present and future.

For personal finance beginners, learning the basics of budgeting, saving, debt, investing, risk, and financial goals can improve decision-making over time. Use reliable sources, question unrealistic promises, apply what you learn, and continue improving your financial knowledge step by step.

Next: After improving your financial knowledge, the next step is to use financial technology and digital money tools wisely while protecting your personal and financial information.

Step 7: Use Financial Technology and Money Tools Wisely

Financial technology has made managing money faster and more convenient. Today, you can check your bank balance, track expenses, pay bills, create a budget, invest, and monitor financial goals using a smartphone. However, technology is only useful when it helps you make better decisions instead of encouraging unnecessary spending or creating security risks.

For personal finance beginners, financial tools can simplify money management by organizing financial information in one place. A budgeting app may show where your money goes, an expense tracker may help identify unnecessary spending, and an automated transfer can make saving more consistent.

However, no app can automatically create good financial habits. A tool can show that you spent too much, but you still need to decide what to change. Use technology as a support system—not as a replacement for financial knowledge and personal responsibility.

How Financial Technology Can Help You Manage Money

Different financial tools are designed for different purposes. You do not need to install every app. Choose tools that solve a specific problem in your financial life.

| Financial Tool | How It Can Help | What to Check |

|---|---|---|

| Banking App | Check balances, review transactions, transfer money, and pay bills | Security settings and transaction alerts |

| Budgeting App | Plan monthly income and expenses | Privacy policy and data access |

| Expense Tracker | Identify spending patterns | Accuracy and account permissions |

| Goal Tracker | Monitor progress toward savings goals | Whether the goals are realistic |

| Investment Platform | View investments and research products | Fees, risks, and regulatory information |

| AI Financial Tool | Organize information and explain financial concepts | Accuracy, privacy, and limitations |

The best financial tool is not always the one with the most features. It is the one you can understand, use consistently, and trust with your information.

Use Budgeting and Expense-Tracking Tools to Understand Your Spending

Many people know their monthly income but cannot clearly explain where all their money goes. Small expenses can become difficult to notice when they happen through digital payments.

An expense tracker can help you categorize spending, such as:

- Rent or housing

- Food and groceries

- Transportation

- Mobile and internet bills

- Entertainment

- Shopping

- Loan or EMI payments

- Savings and investments

For example, suppose your monthly income is ₹25,000. You believe that you spend only ₹2,000 on online shopping and food delivery. After tracking your expenses for one month, you discover that the actual amount is ₹4,500.

The tool did not create the problem. It simply made the spending pattern visible. You can now decide whether reducing that category would help you save more.

If you are earning regularly but still struggle to save, read our guide on why you can’t save money even with a good salary. It explains hidden spending habits and practical ways to improve your savings.

Use Automation to Make Saving More Consistent

Automation can reduce the need to make the same financial decision every month. For example, you may schedule an automatic transfer to a savings account shortly after receiving your income.

Suppose you earn ₹30,000 per month and want to save ₹3,000. Instead of waiting until the end of the month to see what remains, you may automatically move ₹3,000 into savings after your income arrives.

| Without Automation | With Automation |

|---|---|

| Save whatever remains at the end of the month | Move a planned amount soon after receiving income |

| Saving may be affected by unnecessary spending | Savings become part of the monthly system |

| Requires a new decision every month | Reduces repeated manual effort |

Automation should still be reviewed regularly. If your income changes or you have an unexpected expense, you may need to adjust the amount.

Use AI Tools as Financial Assistants, Not Financial Decision-Makers

AI tools can help explain financial terms, summarize information, create a basic budget template, organize expenses, compare general financial concepts, and generate questions for research.

For example, you can ask an AI tool:

- “Help me create a monthly budget using an income of ₹25,000.”

- “Explain the difference between saving and investing in simple language.”

- “Create a checklist for comparing two financial products.”

- “Help me identify possible unnecessary expenses from this spending list.”

However, AI-generated information can be incomplete, outdated, or incorrect. Do not treat an AI response as personalized financial advice. Verify important information using official sources before making major decisions.

For a detailed overview, read our guide on 10 Best AI Tools to Manage Your Personal Finances in 2026. It explains how AI tools may support budgeting, expense tracking, financial planning, and money management.

Protect Your Financial Information

Convenience should not come at the cost of security. Financial apps may contain sensitive information, including account details, transaction history, personal information, and spending patterns.

Before installing or connecting a financial app, check what information it requests and why it needs that access.

Follow these basic security practices:

- Use a strong and unique password for important financial accounts.

- Enable two-factor authentication when available.

- Keep your phone and financial apps updated.

- Do not share OTPs, passwords, PINs, or security codes.

- Avoid entering financial information on suspicious websites.

- Review app permissions before connecting bank accounts.

- Turn on transaction alerts when available.

- Log out of financial accounts on shared devices.

The Cybersecurity and Infrastructure Security Agency’s Secure Our World guidance provides practical information about strong passwords, multi-factor authentication, software updates, and recognizing phishing attempts.

Check Privacy Before Connecting Your Financial Accounts