hi my name is mr khan iam content writer I have experience 🙂 last 3 year❤️

Asif Khan

Planning in India: A Complete Guide (2025)

Early retirement is no longer just a dream for the rich — it has become a clear and achievable financial goal for millions of Indians. With rising stress in corporate jobs, increasing awareness about financial independence, and the 💹 of smart investment options, more people now want to retire at 40 or 45, instead of waiting till 60https://www.iciciprulife.com/retirement-pension-plans/early-retirement-planning-tips..

But achieving early retirement in India requires one thing: a clear plan.You must know how much money you need, where to invest, how to grow your income, and how to protect your savings from inflation. The good news is that with the right strategy, even a middle-class person can retire early and live a peaceful, financially secure life.

Early retirement means stopping regular job/work before the age of 60 and living fully from your savings, investments, and passive income.Today, many Indians aim to retire at 40–45 instead of 60.

. Why Early Retirement Is Becoming Popular

People want:

More freedom

Time for family

Time to build a business

Break from corporate stress

Financial independence

Early retirement gives you choice + control + peaceful life.

3. Calculate Your “Retirement Number”

Before planning, you must know: How much money do I need to retire early?

hii my name is asif iam content writer i have experience 🙂 last 3 year contant writing

Asif Khan

Asif Khan

Introduction: From Saver to Smart Investor

2025 Investors Mutual Fund: Your Essential Blueprint for Building wealth In today’s dynamic financial landscape, simply saving 🤑 is not enough to stay ahead of inflation. Mutual funds have emerged as the premier vehicle for wealth creation, offering diversification and professional management to retail investors. This comprehensive guide cuts through the complexity, providing you with a clear, step-by-step blueprint to understand, select, and manage mutual funds effectively. By the end of this article, you will be equipped with the knowledge to make informed decisions that align with your unique financial goals.https://www.mnclgroup.com/long-term-investing-beginners-blueprint-for-wealth-building

A mutual fund is essentially a financial intermediary—a trust that collects money from a large number of investors with similar investment objectives. This pooled capital is then invested in various assets by a professional fund manager. The Key Players in Your Investment

The Key Players in Your Investment

•The Investor (You): The individual buying the fund units, aiming for growth or income.

•Asset Management Company .(AMC): The institution (or fund house) that launches and manages the fund schemes.

Fund Manager: The expert who actively researches and decides what to buy and when to sell, based on the fund’s mandate.

Custodian: A separate entity that holds the fund’s securities safely, ensuring investor protection.

: How Returns are Generated

Your investment grows primarily through two mechanisms:

Capital Appreciation: When the value of the underlying stocks or bonds in the fund’s portfolio increases.

Income Distribution: Interest (from bonds) or dividends (from stocks) earned by the fund are distributed to the unit holders.

Successful investing is a journey, not a sprint. Follow this structured approach to ensure your mutual fund choices are robust and resilient.

3: Step 1: Goal Setting and Risk Profiling

This is the most crucial preliminary step. You must link every investment to a specific, quantified goal (e.g., ₹20 Lakh in 10 years for a child’s education).

Goal Horizon:

Short-Term (1-3 years): Park funds in safer Debt Funds or Liquid Funds

Long-Term (7+ years): Allocate a higher percentage to Equity Funds to benefit from compounding.

Debt Funds: Ideal for capital preservation and stable income. Example: Liquid Funds, Corporate Bond Funds.

Hybrid Funds: Provide a mix of equity and debt for balanced growth. Example: Aggressive Hybrid Funds.

H3: Step 3: Direct Plan vs. Regular PlanAs a smart investor, always consider the impact of fees over time:

3: Step 4: Investment Methodology (SIP vs. Lumpsum)

Systematic Investment Plan (SIP): Recommended for salaried individuals. By investing a fixed amount regularly, you automatically practice Rupee Cost Averaging, buying more units when prices are low and fewer when prices are high, thereby reducing market timing risk.

Your job doesn’t end after investing. Review your portfolio every 6-12 months.

•Portfolio Rebalancing: Adjust your asset allocation back to its original target (e.g., if Equity has grown too large, sell some and move to Debt).

Performance Check: Compare your fund’s return against its Benchmark Index and its peer group. If it consistently underperforms the benchmark over 3-5 years, consider switching.

2: Due Diligence: What Makes a Fund a Good Investment?

3: Critical Evaluation Metrics

1•Expense Ratio: The lower the fee, the better. Always verify the expense ratio of the Direct Plan.

2:Fund Manager‘s Experience: Look for a manager with a long tenure and a proven track record of navigating both bull and bear markets. Stability is key.

3:Alpha and Tracking Error:Alpha: The excess return generated by the fund over its benchmark. A consistently positive Alpha shows the manager’s skill.

Tracking Error (Passive Funds): How closely an index fund tracks its index. Lower tracking error is better.

4:Tax Efficiency: Be aware of the tax implications (LTCG vs. STCG) before redeeming, especially for goal-based investments.

👇📄✍️Conclusion: Discipline is the Ultimate Fund Manager

Investing in mutual funds is a powerful strategy, but it requires patience and discipline. Start small, stay committed to your SIPs, and focus on the power of compounding over the long term. Remember, the goal is not to get rich quickly, but to get rich surely.

Post Summary (Concise) The article serves as an essential blueprint for smart mutual fund investing. It outlines the strategic steps required to maximize long-term wealth while minimizing risk.

Key Takeaways:Foundation: Successful investing starts with linking capital to specific financial goals and correctly assessing your risk tolerance.

Efficiency: Always choose the Direct Plan over the Regular Plan to benefit from a significantly lower Expense Ratio and higher long-term returns.

Due Diligence: Evaluate a fund based on its consistent performance against its Benchmark, the manager’s track record, and the long-term tax implications (LTCG).

Call To Action

Click here to change this text. Lorem ipsum dolor sit amet, cok

hii my namr is mister iam content writer 3 year experience

Asif Khan

The FIRE Mindset: How the Middle Class Can Achieve Financial Freedom and Retire Early

Most middle-class people work their whole lives hoping to retire at 60 — but by that time, they’re tired, stressed, and still paying EMIs.Yet there’s a growing global movement that challenges this old idea — it’s called FIRE, which stands for Financial Independence, Retire Early.

The goal of FIRE isn’t just to stop working early — it’s to gain freedom.Freedom from financial stress, from depending on a job, and from living paycheck to paycheck.And yes, even an ordinary middle-class person can achieve it with the right mindset and plan.

The middle class often follows one formula all their life:Earn → Spend → Pay EMIs → Repeat.

This endless loop keeps them dependent on their salary.The main problems are:

lack of mindset

Lack of financial educationFear of risk and investmentLifestyle inflation (spending more when income increases)No long-term wealth planTo break free, you need to think differently — not like a consumer, but like an investor.

📊 Step 1: Know Your Financial Freedom Number

Before you plan early retirement, find your Freedom Number — the total wealth you need to live comfortably without working.

formula

Formula:Monthly Expenses × 300 = Freedom Number

examle

If your average monthly expense is ₹30,000→ ₹30,000 × 300 = ₹90,00,000

📈 Step 3: Start Investing Early — Let Compounding Work for You

Saving doesn’t make you rich — investing does.Start small, but start early.

Smart FIRE Investments:

Index Funds / ETFs – Safe, long-term wealth compounding

Mutual Funds (SIP) – Perfect for middle-class investors

Dividend Stocks – Create steady passive income

REITs / Digital Assets – Low-maintenance real-estate income

If you invest ₹10,000 per month at 12% annual return for 20 years —you’ll have over ₹1 crore. That’s the power of compounding!

💼 Step 4: Build Multiple Streams of Income

One salary = one point of failure.To retire early, you need multiple income sources.

Side Income Ideas for the Middle Class:

Start a blog or YouTube channelFreelance in your skill areaCreate an online course or eBookDo affiliate marketingRent out a room or property

Even ₹5,000–₹10,000 extra per month can speed up your FIRE journey.

🔁 Step 5: Reinvest and Automate Your Growth

Don’t spend your profits — reinvest them.Let your money keep multiplying quietly.Automate SIPs, recurring deposits, and side-hustle savings.The goal: build a self-sustaining system where money grows without constant attention.

🕊️ The True Meaning of Early Retirement

Early retirement doesn’t mean sitting idle.It means having the freedom to work on what truly inspires you — without worrying about monthly bills.

🌱 Final Thoughts

You don’t have to be born rich to retire early.You just need to think smart, start early, and stay consistent.

✅ Quick Recap

Step Focus Goal

1 Find your Freedom Number Set your target wealth2 Save 40–60% income Build capital fast3 Invest early & consistently Harness compounding4 Add extra income streams Increase financial speed5 Reinvest profits Achieve long-term freedom

High-Growth Industries Every Investor Must Watch in 2025 is shaping up to be a year full of investment opportunities for those looking to grow their wealth. Certain high-growth industries are emerging as the most promising avenues for smart investors. Sectors like Technology & AI, Renewable Energy, Healthcare & Biotechnology, E-Commerce & Digital Services, and Electric Vehicles (EVs) are driving innovation and delivering significant returns.

Understanding why these sectors are booming, who the key players are, and the performance numbers behind them is crucial for making informed investment decisions. In this blog, we break down 5 top sectors, highlighting market trends, growth drivers, and investment potential, giving you a clear roadmap for 2025. 📊

AI, cloud computing, cybersecurity, and software innovations are reshaping industries globally. Automation, analytics, and smart solutions are driving demand.

2. Key Players / Investors:

Major players include Microsoft, Google, Nvidia, and innovative AI startups. Venture capital and tech-focused funds are heavily investing in AI technologies.

3. Growth Reasons:

Increasing automation in enterprises Rising adoption of AI-driven analytics and cloud services High demand for cybersecurity solutions

4. Performance Numbers:

Global AI spending projected to reach $154B in 2025

EVs, battery technology, charging infrastructure, and autonomous vehicles are leading the mobility revolution. ⚡

2. Key Players / Investors:

Tesla, BYD, Tata Motors, CATL, and EV-focused venture capital.

3. Growth Reasons:

Government EV incentives and climate policiesRising fuel prices and consumer demand for eco-friendly vehiclesBattery technology innovation reducing costs

4. Performance Numbers:

Global EV market projected $1T by 2025CAGR: 22% (2022–2025)EV sales up 40% YoY in China & Europe (2024)

These 5 high-growth industries offer strong investment potential in 2025. By focusing on Technology & AI, Renewable Energy, Healthcare & Biotech, E-Commerce & Digital Services, and EVs, investors can capitalize on rapidly growing markets and make informed investment decisions. Always combine emerging sectors with stable investments for a balanced and profitable portfolio. 💡

These 5 high-growth industries offer strong investment potential in 2025. By focusing on Technology & AI, Renewable Energy, Healthcare & Biotech, E-Commerce & Digital Services, and EVs, investors can capitalize on rapidly growing markets and make informed investment decisions. Always combine emerging sectors with stable investments for a balanced and profitable portfolio. 💡

Diwali is not just a festival of lights — it’s a festival of new beginnings and wealth creation.While most people clean their homes and decorate their surroundings, smart investors clean their financial portfolios and prepare for the next year’s growth.

As India enters 2025 with strong economic momentum, many mutual fund investors are asking one big question:👉 “Which sectors will deliver the best returns in 2025?”

1️⃣ Banking & Financial Services – The Backbone of India’s Growth

The financial sector remains the strongest pillar of India’s economy.After the 2024 interest rate cycle and growing digital adoption, this sector is set to deliver consistent gains in 2025.

Why it will perform well:

Strong credit growth 📈 due to economic expansionDigital banking and UPI adoption rising rapidly Government’s financial inclusion initiatives

Infrastructure & Capital Goods – The Engine of Development

With the government’s continuous push on “Make in India” and “Viksit Bharat 2047”, infrastructure remains a long-term growth 💹 story.Roads, bridges, power plants, and housing projects are set to multiply in 2025.

Why it will perform well:

Rising public and private capex (capital expenditure)Boost in manufacturing and real estateGlobal companies shifting production to India

Top Mutual Funds to Watch:

Kotak Infrastructure & Economic Reform FundNippon India Power & Infra Fund

3️⃣ Renewable Energy & Electric Vehicles – The Future Is Green

The world is moving toward sustainability, and India is leading the green revolution.Renewable energy, EV infrastructure, and green hydrogen are the next multi-decade growth engines.

Why it will perform well:

Strong government incentives and budget allocationRising EV adoption and charging infrastructureGlobal investors backing Indian clean energy startups

Top Mutual Funds to Watch:

Tata Resources & Energy FundAditya Birla Sun Life New Energy Fund

4️⃣ Technology & Digital Transformation – Innovation Never Sleeps

After a correction in the last few years, the Indian IT and tech sector is regaining strength.With AI, cloud, and fintech booming, 2025 might mark a strong comeback

Why it will perform well:

Rising demand for automation and digital toolsAI-led productivity growth in companiesNew wave of Indian tech startups and global contracts

5️⃣ Healthcare & Pharma – The Steady Wealth Builder

Health awareness, medical tourism, and export growth are giving India’s pharma sector a second wind.While not flashy, it offers reliable returns and portfolio protection.

Why it will perform well:

Rising healthcare spending across India Demand for generics in global markets Stable margins and consistent 💹 groth

Top Mutual Funds to Watch:

Nippon India Pharma Fund Mirae Asset Healthcare Fund

pro tip👇

💡 Pro Tip: Best suited for defensive investors who prefer stability over high risk.

🌟 Conclusion: Invest in Sectors That Light Up Your Future🤑👇

Just as Diwali brings light to our homes, smart investments bring light to our financial future.Don’t invest emotionally — invest strategically. Diversify your portfolio across multiple sectors to balance risk and growth.✨ Let your money celebrate Diwali too — not with firecrackers, but with compounding returns.

📊 Call to Action (CTA):

💼 This Diwali, review your portfolio and add mutual funds that align with India’s growth story.🔍 Always consult a financial advisor before making new investments.🎇 Start a SIP this festive season — because the best gift you can give yourself is financial freedom.

💡 “The difference between successful people and really successful people is that really successful people think differently.” — Warren Buffett

Top 7 Mental Models Investors Use Worldwide (Like Warren Buffett)

If you truly want to create wealth like Buffett or Munger, forget chasing the next hot stock.Instead, master the mental models — the hidden thinking frameworks that billionaires quietly use to make smarter, safer, and faster investment decisions

These models work even if you start small — say with ₹5,000 or ₹10,000.Let’s dive deep into the 7 Rich Mental Models that can transform your investing mindset forever.

🧠 1️⃣ Circle of Competence — Invest Only in What You Understand

what it is

Your Circle of Competence is the area where you genuinely understand how things work — products, businesses, or industries you know inside-out.

⚙️ How It Works:

Warren Buffett and Charlie Munger stay inside their circle.If they don’t understand a business (like crypto or biotech), they simply skip it.Their rule is: “It’s not important how big your circle is — what matters is knowing where its boundary lies.”

💡 How You Can Use It (with ₹5,000–₹10,000):

1. Make a list of products or companies you personally use (like HDFC Bank, Zomato, or Maruti).

💸 2️⃣ Margin of Safety — Protect Your Downside First

🔍 What It Is:

https://groww.in/blog/margin-of-safety Your Circle of Competence is the area where you genuinely understand how things work — products, businesses, or industries you know inside-out.

⚙️ How It Works:

Warren Buffett and Charlie Munger stay inside their circle.If they don’t understand a business (like crypto or biotech), they simply skip it.Their rule is: “It’s not important how big your circle is — what matters is knowing where its boundary lies.”

₹10,000 invested at 15% per year = ₹40,456 in 10 years,and ₹1,62,889 in 20 years — without adding a single rupee more.

💡 How You Can Use It (with ₹5,000–₹10,000):

1. Start an SIP in a quality stock or index fund.2. Reinvest all profits (don’t withdraw).3. Stay invested for the long term.✅ Result: Your patience turns into profit. The longer you wait, the bigger your reward.Tata Capital IPO 2025: 10 Quick Points You Must Know

4️⃣ Inversion Thinking — Win by Avoiding Mistakes

🔍 What It Is:

Charlie Munger’s secret weapon: “Invert, always invert.”Instead of asking “How can I get rich?”, ask “What makes people lose money?” — and avoid it.

⚙️ How It Works:

Avoiding stupidity often beats chasing brilliance.Most investors lose because they overtrade, panic, or follow hype.

💡 How You Can Use It (with ₹5,000–₹10,000):

1. Don’t buy anything you don’t understand.2. Avoid emotional investing.3. Keep a personal list: “My Top 3 InvestingMistakes to Avoid.”✅ Result:

🧮 5️⃣ Opportunity Cost — Every Rupee Has a Smarter Use

what it is

Opportunity cost means understanding that choosing one option always means giving up another potentially better one.

How it work

If Stock A gives 10% return and Stock B gives 15% with similar risk — that 5% is your missed opportunity.

💡 How You Can Use It (with ₹5,000–₹10,000):

1. Always compare options before investing.2. Don’t park your money in low-return assets for long.3. Ask: “Is this the smartest use of my ₹5,000?”✅ Result: You start investing where your money works the hardest.

—🔮 6️⃣ Second-Order Thinking — See What Others Can’t

what it is

Average investors see only the first effect of a decision.Great investors see the chain reaction — the second, third, and fourth effec

How it work

Example:“If AI automates jobs, which companies will benefit from that shift long-term?”Thinking one step deeper gives you an early edge.

💡 How You Can Use It (with ₹5,000–₹10,000):

Analyze future consequences of current trends.2. Study how one industry affects another.3. Don’t react to news — think beyond it.✅ Result: You’ll see tomorrow’s winners before others even notice them.

🌟 Final Thought: The Mind Builds Wealth Before the Market Does

Money follows clarity of thought, not luck.If you master these 7 mental models, you’ll start thinking like a millionaire even before you become one.👉 Start small, stay consistent, and let your mind — not the market — do the heavy lifting.

🧩 Conclusion:

Every great investor — from Warren Buffett to Charlie Munger — built wealth not just with money, but with mental discipline.These 7 mental models are not just “investing tricks.” They are ways of thinking that keep you calm when others panic, patient when others rush, and confident when others doubt.

Are you looking for investments that can truly outperform the broader market and deliver highly focused returns? If so, then understanding Thematic Mutual Funds in India32% Returns in Last 5 Years (Outperforming)” is essential. These funds have proven their potential by targeting powerful, future-ready sectors, with many schemes delivering up to an astonishing 32% returns over the last five years. However, navigating the many available options can be a challenge. In this guide, we cut through the confusion to present the Top 7 Thematic Mutual Funds in India that have consistently beaten their peers, helping you answer three core questions:

1. Theme-Based Investing – These funds focus on a specific sector or theme (like Technology, Banking, Energy, or Healthcare).

2. High Risk–High Return –

When the theme performs well, returns can shoot up to 30–35% CAGR, but the downside risk is equally high.

3. Best for 3–5 Years Horizon – Suitable

Suitable for short to medium-term growth opportunities, not ideal for long-term core portfolios.

4. Diversification Tip

Limit exposure to 5–10% of your portfolio to capture growth while keeping risks under

1 :Technology Thematic Fund 🚀

💡 Objective: Invests in fast-growing IT, cloud, AI, and digital businesses shaping the future.

📊 Annualised Returns:

1 Year: 8.5%3 Years: 15.7%5 Years: 21.3%

👤 Who Should Invest:

Long-term investors betting on India’s tech boomRisk-takers looking for high growth in Thematic Mutual Funds in IndiaThose comfortable with short-term volatility⚠️ Risks: Rapid tech disruptions • High volatility • Sector-only exposure

Investors wanting a defensive sector in their portfolioThose looking for steady growth in Thematic Mutual Funds in IndiaLong-term healthcare believers

⚠️ Risks: Regulatory hurdles • High R&D costs • Drug approval delays

3. Infrastructure Thematic Fund 🏗️

💡 Objective: Focuses on roads, power, and India’s mega-development projects.

📊 Annualised Returns:

1 Year: 9.4%3 Years: 17.8%5 Years: 23.6%

👤 Who Should Invest:

Long-term wealth creators (5+ years)Investors betting on India’s growth storyThose seeking higher returns from Thematic Mutual Funds in India

⚠️ Risks: Policy risks • Project delays • High capital exposure

4 Banking & Financial Services Fund 💳

💡 Objective: Invests in banks, NBFCs, insurance & fintech companies.

📊 Annualised Returns:

1 Year: 7.1%3 Years: 16.2%5 Years: 22.4%

👤 Who Should Invest:

Those seeking growth + dividend potential Investors wanting core exposure to India’s financial backbone Thematic Mutual Funds in India lovers focusing on BFSI sector

✅ Conclusion: Thematic Mutual Funds allow investors to ride on specific megatrends like technology, healthcare, and infrastructure. They can deliver 32%+ returns over 5 years, but come with higher risk & volatility compared to diversified funds. Hence, investors should pick them as a satellite allocation (10–20% of portfolio), not as the core portfolio.

Call To Action

✅ Invest Smart, Grow Faster with Thematic Mutual Funds! 🚀 👉 Explore Top Thematic Funds Now 💹 🔎 Discover High-Risk, High-Reward Mutual Funds Today! 📊 📢 Don’t Miss – Top 7 Thematic Mutual Funds in India! 🌍

iam content writer ihve experience and expertise 3 year

Asif Khan

what is flexi cap

FlexiCap Funds are a type of mutual fund that invest across large-cap, mid-cap, and small-cap stocks. These funds give fund managers the flexibility to pick the best stocks based on market conditions. This makes them an ideal choice for middle-class families, offering the potential for 12–15% growth over 5 years while keeping investments diversified.

History of flexicap

FlexiCap Funds are a relatively new type of mutual fund.

Earlier, mutual funds had fixed allocation rules – you had to invest a certain % in large-cap, mid-cap, or small-cap stocks.

FlexiCap Funds were introduced to give fund managers flexibility, allowing them to adjust investments dynamically across all market caps depending on market trends.

Over the last 5–10 years, these funds have become popular among middle-class investors, offering both diversification and good growth potential.

Parag Parikh Flexi Cap Fund is a premium global flexi-cap mutual fund available to investors in India. 🌍 It invests across a wide spectrum of stocks, including large-cap, mid-cap, and small-cap companies, both domestically and internationally. Its primary goal is long-term wealth creation, providing investors exposure to global markets. By combining domestic and international opportunities, this fund allows for portfolio diversification, aiming to balance risk and reward effectively over time.

Key Highlights

This fund follows a value and growth-oriented investment strategy, carefully selecting stocks with strong potential for long-term appreciation. It is particularly suitable for middle-class investors who want to build wealth gradually. Over the last 5 years, the fund has delivered approximately 21.43% CAGR (Check on Moneycontrolhttps://www.monnycontrol.com), making it a consistent performer in its category. Investors benefit from diversification across market caps and exposure to Indian and global equities, which helps balance risk and growth potential.

Why Choose This Fund

Investors prefer Parag Parikh Flexi Cap Fund because it offers a balanced risk-return profile through strategic allocation across domestic and international stocks. Managed by experienced fund managers, the fund emphasizes long-term sustainable growth. With an average 5-year return of 21.43%, it is ideal for investors seeking a well-diversified portfolio, a global perspective, and consistent performance. Its unique blend of value and growth stocks ensures a comprehensive strategy for wealth creation over the years. 💼They Ignored You When You Were Broke — Now They Watch in Silent Jealousy

2. Mirae Asset Flexi Cap Fund

📈 5-Year ReturnThe Mirae AssetFlexi Cap Fund has delivered an impressive ~20% CAGR over the past five years.👉 For example, if someone had invested ₹1,00,000 in 2019, today that amount would have grown to ₹2,48,800+ in 2024. This shows the fund’s power in compounding and wealth creation.

💡 Investment Strategy

The fund primarily invests in Indian equities with a focus on high-growth sectors like Banking, IT, Healthcare, and Consumer Goods. By spreading investments across large-cap, mid-cap, and small-cap stocks, it ensures a balanced mix of stability and aggressive growth. This helps middle-class investors enjoy the growth of India’s economy while minimizing risk from market fluctuations.Best Investment Options for Beginners in India (2025 Guide)

👨👩👧 Ideal For

This fund is ideal for salaried professionals and middle-class families aiming for long-term wealth creation. Even a small SIP of ₹5,000 per month for 5 years could have grown to ₹4.5–5 Lakh+, compared to only ₹3 Lakh invested. This makes it a powerful tool for achieving life goals like children’s education, home purchase, or retirement planninghttps://www.moneycontrol.com/

. #3 JM Flexi Cap Fund

1. Diversified Across Market CapsJ M Flexi Cap Fundinvests in large-cap, mid-cap, and small-cap stocks, allocating funds dynamically based on market trends. For example, if the fund has ₹500 crore invested in large-cap stocks, it might allocate ₹300 crore to mid-cap and ₹200 crore to small-cap to balance risk and returns.

Sectoral Flexibility

The fund shifts investments across sectors like technology, finance, healthcare, and consumer goods depending on growthopportunities. This flexibility allows ₹100–₹200 crore to move into high-growth sectors without affecting overall portfolio stability.https://www.moneycontrol.com/

Dynamic Risk Management

JM Flexi Cap Fund adjusts its portfolio according to market volatility. During uncertain times, the fund may increase allocation to safer large-cap stocks and reduce exposure in small-cap stocks, ensuring that the investor’s ₹1 lakh SIP or ₹5 lakh lump sum is protected while still aiming for growth.“7 Proven Ways for Small-Town Students to Earn Money Online in 2025 (₹5k–₹50k/Month)”

4. Quant Flexi Cap Fund 🚀

This fund is a flagship offering known for its dynamic and aggressive investment strategy, frequently ranking among the top performers in the Flexi Cap category. It is an ideal choice for investors with a high-risk appetite aiming for accelerated long-term capital growth.

Investment Strategy & Philosophy

The Quant Flexi Cap Fund relies heavily on a Quantitative (Quant) model which uses predictive analytics and market signals, rather than traditional research, to actively manage its portfolio. The fund managers use a flexible approach, aggressively shifting allocation across large, mid, and small-cap stocks based on their proprietary VLRT (Valuation, Liquidity, Risk, and Time) framework. This high-conviction, concentrated approach allows the fund to swiftly capitalise on market volatility and capture significant growth opportunities.

Performance and Key Figures

The The fund has demonstrated sorryty check 🔗http://Quant Flexi Cap Fund Direct-Growth – Latest NAV, Returns, Performance 2025Source: exceptional compounding ability, delivering a high 5-year CAGR of approximately 27.9\%. As of the latest data, its Assets Under Management (AUM) stand at around ₹6,686.67 Crores. An investor can start a Systematic Investment Plan (SIP) with a minimum amount as low as ₹250, making it accessible to most middle-class savers aiming for high returns. has demonstrated exceptional compounding ability, delivering a high 5-year CAGR of approximately 27.9\%. As of the latest data, its Assets Under Management (AUM) stand at around ₹6,686.67 Crores. An investor can start a Systematic Investment Plan (SIP) with a minimum amount as low as ₹250, making it accessible to most middle-class savers aiming for high returns.7 Proven Ways for Students to Make Money

5 PGIM India Flexi Cap Fund 📊

This fund has rapidly gained recognition for its consistent, risk-adjusted returns and a structured investment process focused on generating alpha across market cycles. It appeals to investors seeking a balance of aggressive growth potential and strong downside protection.https://www.pgimindia.com/mutual-funds/equity-funds/flexi-cap-fund

Investment Strategy & Philosophy

The PGIM IThe PGIM India Flexi Cap Fund adheres to a disciplined GARP (Growth at a Reasonable Price) philosophy. The fund managers focus on identifying high-quality businesses with strong governance and a proven track record of earnings growth, but only when they are available at attractive valuations. The strategy involves a rigorous 3-step investment process—Idea Generation, Fundamental Research, and Portfolio Construction—ensuring that capital allocation is based on deep analysis rather than market sentiment. This balanced approach helps the fund remain resilient during volatile market phases.adheres to a disciplined GARP (Growth at a Reasonable Price) philosophy. The fund managers focus on identifying high-quality businesses with strong governance and a proven track record of earnings growth, but only when they are available at attractive valuations. The strategy involves a rigorous 3-step investment process—Idea Generation, Fundamental Research, and Portfolio Construction—ensuring that capital allocation is based on deep analysis rather than market sentiment. This balanced approach helps the fund remain resilient during volatile market phases.

Performance and Key Figures

The fund has demonstrated its efficacy by delivering a robust 5-year CAGR averaging around 21\%, positioning it well above the category average. The total size of the fund, or its Assets Under Management (AUM), currently stands at approximately ₹8,500 Crores (Note: AUM figures are subject to daily market fluctuations). For investors initiating a Systematic Investment Plan (SIP), the minimum investment requirement is generally ₹1,000, making this high-quality, high-growth fund accessible to a wide range of investors.Best Investment Options for Beginners in India (2025 Guide)

The fund employs a rigorous bottom-up stock selection approach, primarily focusing on acquiring high-conviction, quality stocks irrespective of their market size (large, mid, or small-cap) or sector. The fund seeks out companies with solid fundamentals, experienced management, and a high potential for compounding wealth over a long period. This disciplined, long-term approach makes it suitable for conservative investors with an investment horizon of five years or more. The portfolio is often seen as less volatile than many of its aggressively managed peers.

Performance and Key Figures

Known for its consistent performance across various market cycles, the fund has given a respectable 5-year CAGR of approximately 18.16\%. It is one of the largest funds in the Flexi Cap space, managing substantial Assets Under Management (AUM) of roughly ₹25,500 Crores. You can initiate a SIP in this quality-focused fund with a minimum monthly investment as low as ₹500. Sorsehttps://www.utimf.com/mutual-funds/uti-flexi-cap-fund-formerly-known-uti-equity-fund

Call To Action

Click 📌 Call to Action 💡 Looking for steady long-term growth? FlexiCap Funds can give you 12–15% returns in 5 years. Perfect for middle-class families aiming for wealth building. 👉 Start investing today and secure your financial future!

🚀 Don’t let your savings sit idle! FlexiCap Funds deliver consistent growth with smart strategies. With 12–15% 5-year performance, your money works harder for you. 👉 Invest now and achieve your financial goals faster!

In today’s fast-paced life, having a steady monthly income is crucial. Investing in the right schemes can help you earn ₹5,000, ₹10,000, or more every month while keeping your money safe. These monthly income schemes provide fixed and reliable returns, helping you manage expenses and secure your financial future. Here are the top 7schemes to start earning consistent monthly income.

Higher Interest Rate SCSS generally offers around 8.2% p.a. (2025 rate approx). For example, if you invest ₹1,00,000, you can earn about ₹8,200 per year as interest. Bigger deposits like ₹10 Lakh can generate ₹82,000 yearly.

#2Quarterly Payouts

The interest is credited every 3 months. So, on an investment of ₹1,00,000, you get around ₹2,050 every quarter. This acts like a steady pension for senior citizens.

3. Government-Backed Safety

Since SCSS is a government scheme, your capital is 100% safe. Even if banks or private firms fail, your ₹1 Lakh or more investment remains fully secure.

4. Capital Protection

At the end of the maturity period (5 years, extendable to 8 years), your full deposit (say ₹1,00,000) is returned along with all the interest you earned during the years.

#2Post Office Monthly Income Account (POMIA)

By depositing ₹50,000 to ₹4,50,000, you can earn a fixed monthly interest. For example, a deposit of ₹1,00,000 could give you approximately ₹750–₹800 per month. Your principal is safe, and you enjoy a regular income without any hassle.

2. Monthly Income Scheme (MIS)

The Monthly Income Scheme allows you to deposit ₹1,500 to ₹4,50,000 and get monthly income directly into your account. For example, a ₹2,00,000 deposit can provide around ₹1,000 per month, making it ideal for pensioners or small investors.

3. Kisan Vikas Patra (KVP)

Invest ₹10,000 or more in KVP and watch it grow over the fixed tenure. While the maturity amount comes after a few years, it can be used to generate regular monthly income, roughly ₹500–₹1,000 per month, depending on your planning. This is great for farmers or small investors seeking safe returns.

4. Sukanya Samriddhi Yojana (SSY

Invest ₹1,000 to ₹1,50,000 annually in SSY for your daughter’s future. The scheme accrues interest and can be planned to provide monthly financial support later. For example, a cumulative investment of ₹2,00,000 can give a monthly benefit of ₹1,500–₹2,000, securing both savings and regular income.

Corporate FDs are issued directly by companies instead of banks. You have to invest through the company’s office or authorized partners, which often helps you get higher interest rates compared to bank deposits.

2Income Alone

This scheme is designed to provide a steady monthly income. For example, if you invest ₹5,00,000, at an 8–10% annual interest rate, you can earn around ₹3,500–₹4,200 every month.

3 Monthly Payout Option

Corporate FDs allow you to choose payout frequency—monthly, quarterly, or yearly. If you select the monthly option, the company credits a fixed amount to your account every month, ensuring regular income.

4 Higher Returns

Compared to bank FDs, corporate FDs generally offer higher returns. However, they carry slightly more risk since repayment depends on the company’s financial health. Always choose AAA or high-rated companies for safer investments.How to Save Money as a Student: Beginner Guide in 2025

#4 Corporate Fixed Deposits

Corporate Fixed Deposits (FDs) are investment instruments issued by companies that can offer higher returns than bank FDs. Here is the information presented professionally with numbered points and financial figures:

1Higher Returns: Corporate FDs

offer a 1% to 3% higher return compared to bank FDs. For example, a bank FD might offer a 6.5% return, while a corporate FD could yield 8.5%.fds

Monthly Income Option: Many corporate

FDs provide a monthly payout option. If you invest ₹5,00,000 at an annual return of 8.5%, you could receive a fixed mounthly income of approximately ₹3,542

3Investment & Risk:

: It is essential to check a company’s credit rating before investing. Companies with high ratings like AAA or AA+ are considered the safest. However, they always carry slightly more risk than bank .fds.

Investment Amount & Term:

start investing in corporate FDs with amounts as low as ₹5,000 and can choose a term from 1 to 5 years as per your convenience.

Conclusion:

Corporate FDs are a good option for investors who seek returns higher than bank FDs and are willing to take on a moderate level of risk.easy money for busy students

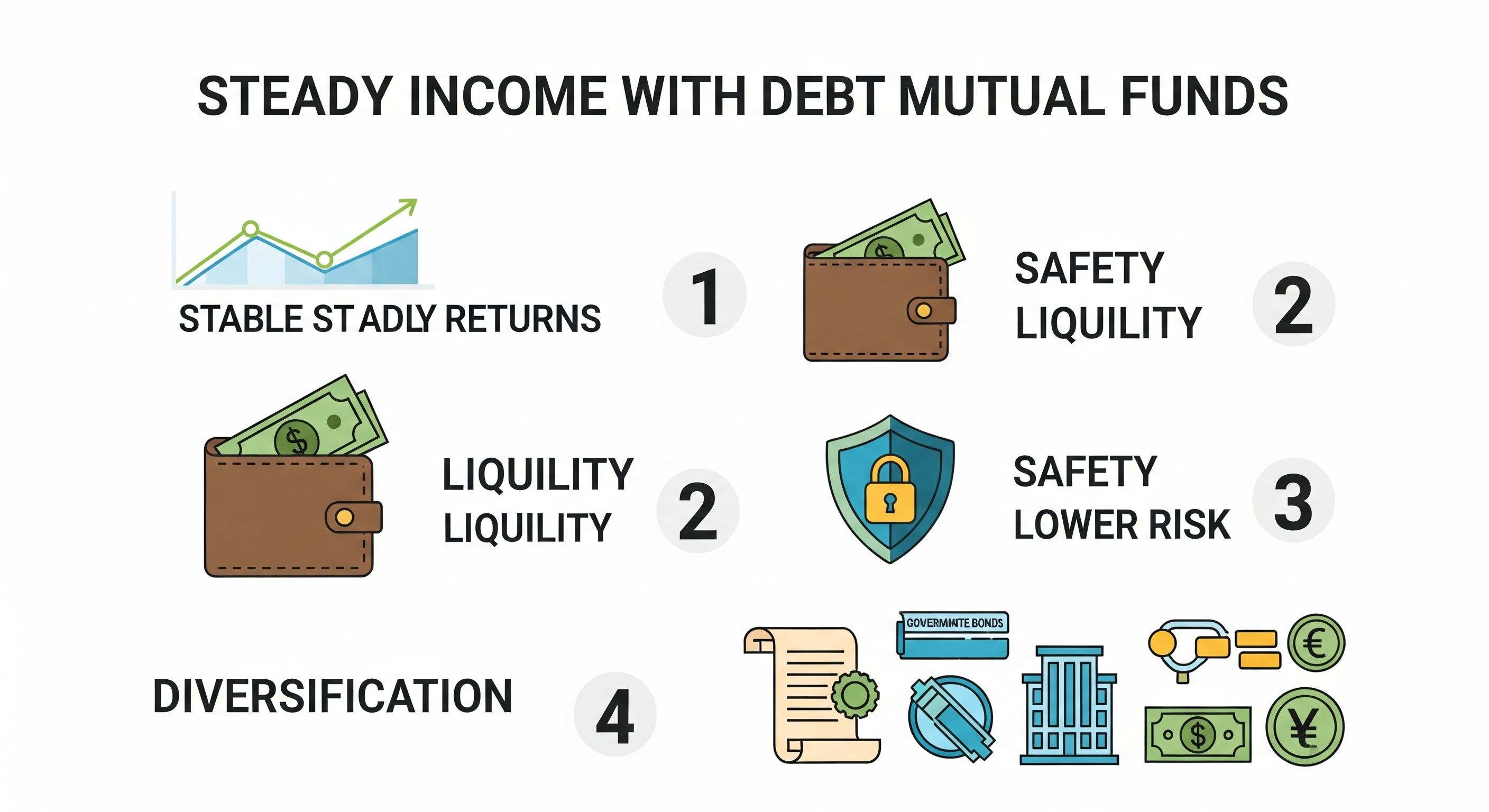

#5Debt Mutual

Mutual Funds:Steady Income: Debt Mutual Funds aim to provide a steady income stream by investing in fixed-income securities like bonds. This makes them a great option for investors who are looking 1for a regular return without the volatility of the stock market.

2 Safety AND Risk

Safety and Risk: They are generally considered safer and less risky than equity (stock) funds. While they are not risk-free, they offer a good balance between safety and returns, making them a suitable choice for conservative investors.

3High Liquidity

Unlike fixed deposits that have a lock-in period, most Debt Mutual Funds offer high liquidity. This means you can easily withdraw your money at any time, often within 1-3 working days, without any penalty.Best Investment Options for Beginners in India (2025 Guide)

Pradhan Mantri Vaya Vandana Yojana (PMVVY)

The Pradhan Mantri Vaya Vandana Yojana (PMVVY) is a government-backed pension scheme specifically designed for senior citizens. It offers a guaranteed return and a steady stream of income to provide finence Security in their later years.

1Guaranteed Pension:

The scheme provides a guaranteed pension for 10 years. The interest rate is fixed at the time of investment, which ensures your income is not affected by market fluctuations. For instance, the current interest rate is approximately 7.4% p.a. (as of 2025).

Your Attractive Heading

2Investment Limits:

An individual can invest a maximum amount of ₹15 Lakh in this scheme. This can be investment made in a single lump sum or in multiple installments. The minimum investment amount required to get a pension of ₹1,000 per month is ₹1,56,658.

3 Flexible Pension Payouts:

You can choose to receive your pension monthly, quarterly, half-yearly, or yearly, depending on your needs. For example, if you invest ₹15 Lakh, you can receive a pension of approximately ₹9,250 every month for the entire 10-year period.

4Early Exit and Loan Facility:

The scheme also includes provisions for premature exit in special circumstances, like a critical illness. Additionally, you can avail of a loan against the policy after 3 years of investment. The maximum loan amount is 75% of the purchase price.

5 Return of Purchase Price:

At the end of the 10-year policy term, the original investment amount (purchase price) is returned to the investor. If the policyholder passes away during the term, the purchase price is paid to the nominee.

7How a Systematic Withdrawal Plan (SWP) Works

1. Creating a Regular Income

An SWP allows you to create a regular, fixed income from your existing mutual fund investment. This is often used by retirees or individuals who have a lump sum of money and need a steady cash flow.

2. Your Investment as the Source

The money you receive each month isn’t just interest. It is a combination of your initial investment and the returns it has generated. Essentially, you’re withdrawing a part of your own capital over a period of time.3. Potential for Continued Growth

3. Potential for Continued Growth

Even as you withdraw money, the remaining amount in the mutual fund stays invested. This means it continues to have the potential to grow, which can help your investment last longer and potentially even increase in value over time.

4. An Example with Numbers

For instance, if you have a ₹10 Lakh investment, you could set up an SWP to withdraw ₹5,000 per month. Over the course of a year, you would receive ₹60,000 in income while the remaining ₹9,40,000 continues to grow in the fund.

Senior Citizen Savings Scheme (SCSS) A government-backed, secure plan for senior citizens that provides a fixed, regular income. Post Office Monthly Income Scheme (POMIS) A low-risk option from the Post Office that offers a steady monthly income. Monthly Income Plan (MIP) A type of mutual fund that balances debt and equity investments to provide a regular income with some potential for growth. Fixed Deposits (FDs) A traditional and secure investment where you can choose to receive your interest earnings on a monthly basis. Corporate Bonds You receive regular interest payments by lending money to a corporation through these bonds. Systematic Withdrawal Plan (SWP) Not a scheme, but a way to get a fixed cash flow by setting up regular withdrawals from your existing mutual fund investment.

Call To Action

Click here I am unable to display the response in a box. I can, however, provide a concise response for you. Senior Citizen Savings Scheme (SCSS): Get a secure, fixed income for your retirement. Invest in SCSS today. Post Office Monthly Income Scheme (POMIS): Looking for a safe and steady monthly income? Start your POMIS investment now. Monthly Income Plan (MIP): Want to earn regular income while growing your money? Explore MIPs. Fixed Deposits (FDs): Turn your savings into monthly earnings. Open a Fixed Deposit with a monthly payout option. Corporate Bonds: Diversify your portfolio and earn regular interest. Consider investing in Corporate Bonds. Systematic Withdrawal Plan (SWP): Need a regular cash flow? Set up an SWP from your mutual fund.

FAQ Ideas for Your Article”What is the minimum investment required for these schemes?””Are these schemes taxable?””How do I choose the right scheme for my age and risk tolerance?””Can I withdraw my money before the maturity period ends?””What is the difference between an FD and a POMIS?””How safe are these investments?”

.

What is FAQ?

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat.

Being a student often means living on a tight budget. But with the right strategies, you can save smartly and still enjoy your lifestyle. 👉 In this Beginner Guide 2025, you will learn: – How to create a simple budget that actually works – Practical ways to cut daily expenses without stress – Smart use of student discounts and offers – Best digital tools & apps to track your money – Side hustle ideas to boost your income This step-by-step guide is designed to help students build financial discipline, avoid common money mistakes, and achieve more with less. Start saving today and take control of your finances in 2025!

Table Of Conte📘 Table of Contents ✨ 1. Introduction ▸ Why saving money matters for students in 2025 💰 2. Create a Smart Budget ▸ Step-by-step guide to track income & expenses ✂️ 3. Cut Down Unnecessary Expenses ▸ Reduce spending on food, gadgets & lifestyle habits 🎓 4. Use Student Discounts & Deals ▸ Unlock hidden savings with student ID & offers 🏠 5. Choose Affordable Living ▸ Hostel vs. shared rooms vs. rentals – smart choices 🥗 6. Save on Food & Groceries ▸ Meal planning, home cooking & discount hacks 📱 7. Use Technology & Money-Saving Apps ▸ Best budgeting apps, cashback & coupon tools 💼 8. Earn Extra Income While Studying ▸ Freelancing, internships & side hustles 🔑 9. Build a Consistent Saving Habit ▸ Small goals → long-term financial stability 🏆 10. Conclusion & Final Tips ▸ Actionable advice & motivation for students

1. Introduction – Why Saving Money Matters for Students in 2025

Being a student in 2025 comes with unique challenges. Education costs, living expenses, and lifestyle pressures are higher than ever. While it may feel difficult to manage finances on a limited budget, learning how to save money early can make a huge difference. Saving money not only reduces stress but also helps students stay focused on studies instead of worrying about expenses. It builds financial discipline, which is an essential life skill for long-term success. In this guide, we will explore practical and realistic ways students can save money in 2025 without sacrificing their lifestyle or academic goals. From budgeting smartly to using student discounts effectively, every step is designed to help students become financially confident.

⭐ The Importance of Saving Early

1️⃣ **Financial Independence** Saving money early gives students freedom. It reduces dependence on parents and builds confidence for real-world responsibilities. —2️⃣ **Avoiding Debt Traps** Consistent savings protect students from credit card bills and loans. Graduating debt-free means a stronger financial start. —3️⃣ **Reducing Stress and Anxiety** Money worries create pressure during studies. An emergency fund lowers stress and keeps focus on academics. —4️⃣ **Unlocking Better Opportunities** Savings open doors to workshops, online courses, and internships. Students can invest in growth without worrying about costs.

2. Create a Smart Budget – Step-By-Step Guide to Track Income & Expenses

Creating a smart budget is one of the most effective ways for students to manage their money wisely. A budget works like a roadmap – it clearly shows where your money is coming from and where it is going. Start by listing all your income sources — like pocket money, scholarships, or part-time earnings. Then, divide your expenses into two groups: – **Fixed expenses** (rent, tuition fees, transport) – **Variable expenses** (food, shopping, entertainment) Once you have this list, set **realistic limits** for each category. Make it a habit to track your spending regularly and review it every month. This simple practice helps you: – Avoid overspending – Identify money leaks – Build long-term financial discipline With a smart budget, you stay in control of your finances and reduce unnecessary stress.

### 3 Key Elements of a Smart Student Budget

1️⃣ Tracking Income & Expenses 📊 Keep a detailed record of your earnings and spending so you always know where your money is going.

2️⃣ Cutting Down Unnecessary Expenses ✂️ Limit extra costs like frequent eating out, gadgets, and lifestyle habits to keep your budget strong.

3️⃣ Using Student Discounts & Deals 🎓 Make the most of student ID offers and discounts to save money on essentials and services.

3. Cut Unnecessary Expenses ✂️ Smart ways to reduce food,

Saving money starts with cutting down on unnecessary expenses. As students, it’s easy to overspend on fast food, trendy gadgets, or impulse purchases that don’t really add long-term value. By tracking where your money goes and removing these extra costs, you can focus on essentials like books, tuition fees, or emergency savings. Practical changes make a big difference: – Cook simple meals instead of eating out every day – Avoid buying items just because they’re on sale – Choose affordable activities that still bring joy Each small adjustment creates a positive impact. The less you waste today, the more financial freedom you’ll build for tomorrow.

Key 🗝️ Point Elements Below

Cut Unnecessary Expenses 🗝️ – Avoid spending on things you don’t really need.

Track Your Spending 🗝️ – Keep a record of every expense to see where your money goes.

Focus on Essentials 🗝️ – Prioritize spending on necessary items like food, books, and study materials.

Practical Changes 🗝️ – Implement habits like cooking at home, using public transport, or sharing resources.

Small Adjustments, Big Impact 🗝️ – Tiny savings daily can grow into significant amounts over time.

Use students discount 🗝️ & deal unlock hidden savings

**Take Advantage of Student Discounts:** Many online stores and apps offer exclusive discounts for students. By verifying your student ID or email, you can enjoy extra savings on every purchase. **Look for Special Deals and Offers:** Every week or month, special deals appear that aren’t available to regular users. These offers can be a great source of hidden savings. **Apply Discounts to Shopping and Study Materials:** Whether you’re buying books, gadgets, or subscribing to apps, combining student discounts with special deals can significantly reduce your expenses. **Save Smartly:** Use every offer and discount strategically to keep your monthly expenses under control. Extra money can be saved for future goals or hobbies. **Maximum Benefit, Minimum Effort:** By following simple steps, you can easily unlock hidden savings and make your student life financially stress-free. The smart saving formula for students is simple: **Use students discount 🗝️ & deal unlock hidden savings!**

Key 🗝️ 5 Student Savings Elements👇

1. Use student discounts – Get exclusive savings on books, apps, and gadgets. 2. Find hidden deals – Extra savings through weekly or monthly offers. 3. Apply discounts smartly – Reduce expenses on shopping and study materials. 4. Save strategically – Keep monthly costs under control. 5. Unlock extra savings – Accumulate money for future goals or hobbies.

5 Choose Affordable Living: Hostel vs Shared Room vs Rental – Smart Choice

When considering affordable living options—hostels, shared rooms, or rentals—it’s essential to evaluate your budget, lifestyle, and preferences. Here’s a comparative overview to help you make an informed decision:🏨 Hostels- Cost: Generally the most budget-friendly option, with dormitory beds averaging around $7 (approximately ₹580) per night.- Ideal For: Students, backpackers, and travelers seeking short-term stays.- Pros: Low cost, social environment, and often include amenities like Wi-Fi and meals.- Cons: Limited privacy, shared facilities, and may not be suitable for long-term stays.🏠 Shared Rooms (Paying Guest or PG)- Cost: More affordable than renting a private apartment, with prices varying based on location and amenities.- Ideal For: Students and working professionals looking for a balance between cost and privacy.- Pros: Semi-private living, often includes meals and utilities, and more comfortable than hostels.- Cons: Shared spaces, less independence, and varying quality depending on the provider.🏡 Rentals (Shared or Private)- Cost: Higher than hostels and PGs, especially in metropolitan areas. For instance, in Chennai, 1BHK rents have nearly doubled over the past two years, with prices now exceeding ₹22,000 in some suburban areas.- Ideal For: Individuals seeking full independence and long-term accommodation.- Pros: Complete privacy, control over living arrangements, and potential for long-term stability.- Cons: Higher costs, responsibility for maintenance, and the need for furnishing.Decision Guide- Budget-Conscious: Opt for hostels or shared rooms to minimize expenses.- Seeking Balance: Shared rooms offer a compromise between cost and privacy.- Prioritizing Independence: Rentals provide autonomy but at a higher cost.In conclusion, your choice should align with your financial capacity, desired level of privacy, and the duration of your stay. For short-term, budget-friendly options, hostels are ideal. For a balance between cost and comfort, shared rooms are suitable. For long-term independence, rentals are the way to go.

Key 🗝️ Elements of Affordable Living Options (Comparison)

6. Save on Food & Groceries: Meal Planning, Home Cooking & Discount Hacks

Saving on food and groceries can be simple and highly effective if done strategically. Start with **meal planning** – by deciding your weekly meals in advance, you avoid buying items you don’t need. This not only saves money but also reduces food waste. Next, focus on **home cooking**. Preparing meals at home is much cheaper than eating out or ordering takeaway. It also allows you to control the ingredients, making your meals healthier. Don’t forget **discount hacks**. Look for store deals, cashback offers, coupons, and bulk-buy options. Even small savings on each purchase add up significantly over time. By combining meal planning, home cooking, and smart discount strategies, you can enjoy tasty and nutritious food without overspending. Consistency is key – small, regular efforts lead to big savings.

Key 🗝️ elements 4 point 👇

1. Meal Planning – Plan weekly meals to avoid unnecessary purchases and reduce waste. 2. Home Cooking – Cook at home for healthier and cheaper meals. 3. Discount Hacks – Use store deals, coupons, cashback, and bulk-buy options. 4. Consistency – Regular efforts lead to long-term savings.

💻💰 7 Use Technology & Money-Saving Apps: Best Budgeting Apps, Cashback & Coupon Tools 🛍️📲

💡 **Best Budgeting Apps** Take full control of your money with apps that track income, expenses, and spending habits. Set budgets, reach your savings goals, and get smart insights—all in one place. Financial planning has never been this simple and stress-free! 💸 **Cashback Tools** Earn money back every time you shop, online or offline. Unlock special deals, seasonal rewards, and exclusive offers that make your purchases more rewarding. Watch your savings grow effortlessly with every swipe! 🏷️ **Coupon Tools** Discover endless discounts, promo codes, and special offers. Apply them at checkout to save on groceries, fashion, gadgets, and more. Shop smarter, spend less, and never miss a chance to stretch your budget further!

💰✨ Money-Saving Tools Comparison Guide 📲🛍️

🌟💰 **Money-Saving Tools Comparison** 🌟────────────────────────────── 💡 **Best Budgeting Apps** – **Focus:** Track & manage your money – **Benefits:** Set budgets, monitor spending, reach savings goals – **Best For:** Long-term financial planning & building smart money habits ────────────────────────────── 💸 **Cashback Tools** – **Focus:** Earn money back on purchases – **Benefits:** Instant cashback, seasonal rewards, exclusive deals – **Best For:** Regular shopping & boosting savings effortlessly ────────────────────────────── 🏷️ **Coupon Tools** – **Focus:** Discounts & promo codes – **Benefits:** Save on groceries, fashion, gadgets, and more – **Best For:** Everyday shopping & stretching your budget further ──────────────────────────────

8. 💸 Earn Extra Income While Studying: Freelance, Internship & Side Hustle 💼

💸 Earn Extra Income While Studying: Freelance, Internship & Side Hustle 💼 Earning extra income while studying has become easier than ever. With the right approach, students can manage their academics while building a steady income stream. **Freelance:** Taking up freelance projects allows you to work on tasks that match your skills. It offers flexibility, so you can choose when and how much you work. This not only brings in money but also helps you develop professional experience and improve time management skills. **Internship:** Internships provide hands-on experience in a real work environment. They help you learn industry practices, build a professional network, and enhance your resume. Even if the pay is modest, the long-term benefits for your career growth are immense. **Side Hustle:** A side hustle lets you turn your hobbies, passions, or creative skills into income. Whether it’s tutoring, content creation, selling handmade products, or offering services online, side hustles teach entrepreneurship, responsibility, and problem-solving while earning extra money. By combining freelancing, internships, and side hustles, you can achieve financial independence, gain practical skills, and prepare yourself for future career opportunities—all while still studying.

Key 🗝️ elements example

### 💻 Comparison Table | Option | Flexibility | Learning | Earning | Example ||————–|————|———|———|————————|| Freelance | High | Medium | Medium-High | Writing, design, coding || Internship | Medium | High | Low-Medium | Marketing, software || Side Hustle | High | Medium | Medium-High | Tutoring, content creation |

9.Build a consistent saving habit 🥍 Set small goals 💡 Aim for long-term financial stability 📈

🥍 Build a Consistent Saving Habit Developing a consistent saving habit is the foundation of financial growth. It helps you manage your money wisely, avoid unnecessary expenses, and create a strong financial routine. Small, regular actions over time can lead to big results, giving you peace of mind and control over your finances.💡 Set Small Goals Start with small, achievable savings goals, like putting aside a fixed amount every week. These mini targets make saving less overwhelming and help you build discipline gradually. Achieving them motivates you to continue and gives a sense of accomplishment every time.📈 Aim for Long-Term Financial Stability Saving consistently with small goals leads to long-term financial stability. It allows you to handle emergencies, plan for big expenses, and secure your future with confidence. Over time, these disciplined habits compound, creating wealth and giving you financial freedom.

3 take point 👇

📚🎯 10. Conclusion & Final Tips: Actionable Advice & Motivation for Students

1. Time Management ⏳ Using time wisely is the key to success. Create a daily schedule and prioritize tasks. This helps you finish more work in less time and stay stress-free. 2. Set & Achieve Goals 🎯 Turn dreams into reality by setting small, clear goals. Every small achievement builds momentum and guides you toward bigger success. 3. Active Learning 📖 Never stop learning. Adopting new skills and knowledge keeps you updated with the times and helps you grow continuously. 4. Celebrate Progress 🎉 Always celebrate small wins. It keeps you motivated and makes your hard work more enjoyable. 5. Seek Support 🤝 Don’t struggle alone. Asking for guidance from family, friends, or mentors makes challenges easier to overcome. 6. Maintain Balance ⚖️ Balancing work and personal life is essential. Mental peace and physical health are your true strengths for long-term success.

Finel key 🗝️ point 👇

🔑 Key Points 1. Manage time with daily schedule & priorities. ⏳ 2. Set small goals to reach big success. 🎯 3. Keep learning new skills actively. 📖 4. Celebrate every small progress. 🎉 5. Take support from family, friends, mentors. 🤝 6. Maintain balance for health & peace. ⚖️

🔥 Quick Summary of 10 Smart Money-Saving Tips 🔥

1️⃣ Cut unnecessary expenses – Say “no” to waste and focus on needs. 2️⃣ Track your spending – Every rupee matters, know where it goes. 3️⃣ Focus on essentials – Prioritize what truly supports your growth. 4️⃣ Make practical changes – Small lifestyle tweaks = big results. 5️⃣ Small adjustments, big impact – Tiny savings add up over time. 6️⃣ Save on food & groceries – Plan meals, cook at home, grab discounts. 7️⃣ Choose affordable living – Hostel, shared room, or budget rental. 8️⃣ Earn extra income while studying – Freelancing, internships, side hustles. 9️⃣ Use smart saving tools – Apps & methods to manage money easily. 🔟 Celebrate progress & stay balanced – Reward yourself, but stay consistent.

Call To Action

Click 🔥 Final Call To Action 🔥 👉 Now it’s your turn! Start applying these 10 smart money-saving tips in your student life today. Remember, small savings can create big financial freedom. 💡 Are you ready to become a smart student and take charge of your money journey? 🔘 If yes, then bookmark this guide and share it with your friends so they can also learn smart money habits. 📩 Want more smart money hacks? 🚀 Subscribe to our FREE newsletter and get weekly money-saving tips & side hustle ideas – straight to your inbox!

👋 Hi, I’m Asif! I’m passionate about personal finance and money management. With 2 years of experience in blogging and exploring smart ways to save, earn, and invest, I help students and young professionals build better money habits. On this blog, you’ll find: 💡 Practical money-saving tips 🚀 Side hustle & earning ideas 📊 Smart financial strategies My mission is simple: To guide you towards financial freedom – step by step, starting today.

Leave a Comment